While researching this guide, I reviewed lender lien procedures, DMV title requirements, IRS guidance on cancelled debt, and dozens of first-hand accounts from vehicle owners who went through this exact situation after their lender never came for the car.

The car loan went unpaid years ago. Nobody ever showed up to tow it. It’s been parked in the same spot since — maybe under a cover, maybe just quietly rusting a little less than you’d expect — and at some point a 1099-C landed in your mailbox. A tax bill followed. That’s the part that never sits right: you lost the loan, and somehow the IRS still wanted a cut.

Why This Situation Confuses So Many People

People get trapped in this loop because they assume the IRS and the DMV talk to each other. They don’t. The IRS only cares whether a cancelled debt should be reported as income. Your state’s DMV only cares who currently holds a legal claim against the vehicle. Two completely separate systems, run by two completely separate agencies, with no shared database between them. That’s the entire reason a 1099-C can land in your mailbox without a single thing changing on your car’s title.

Before You Do Anything, Check These Three Things

You can save yourself a phone call in some cases. Before contacting anyone:

- Is the lien still active? A number of states run an Electronic Lien and Title (ELT) system. Quite a few owners discover they don’t actually need a lien release letter at all, because the lender already reported the release electronically years ago and the DMV’s record has quietly reflected it ever since. Checking your title status online first can save you the call entirely.

- Do you still have the VIN? You’ll need it for every step below.

- Did you actually receive a 1099-C, or did you just stop paying? Only the first one means the lender has formally reported the debt as cancelled.

A Charge-Off Doesn’t Touch the Title. It’s Purely an Accounting Move

A charge-off is a bookkeeping entry. The lender moves your unpaid balance off its books as a loss, for its own financial reporting. That’s it. It has nothing to do with who legally owns the vehicle.

Why Lenders Sometimes Never Repossess the Car

It feels strange that a bank would just leave a vehicle sitting in someone’s driveway for years. It’s actually pretty common with older vehicles that have a serious mechanical problem — but the math behind it is narrower than it sounds. The lender isn’t looking at what the car is worth to a private buyer piecing it out for parts. It’s looking at wholesale auction value, on the day it would repossess, minus towing, storage, and auction fees. If a $600 wholesale car costs $800 to tow, hold, and sell, the lender walks away — even if that same car would bring $1,500 to someone shopping for a transmission or a set of doors. Retail parts value and wholesale auction value are two different numbers, and the gap between them is exactly why a car can be “not worth repossessing” to a bank and still be worth real money to you.

That doesn’t mean the lien goes away. There’s no cost to the lender in leaving it in place, and it protects them if the car ever turns out to be worth something later.

One caution worth taking seriously: a charge-off, and even a 1099-C, doesn’t automatically end a lender’s legal right to repossess in most states. It becomes less common the longer the account sits untouched, but the lien is what actually controls that right — not the tax form.

So Does the 1099-C Cancel the Lien or Not?

No. A 1099-C is an IRS form. It tells the IRS — and you — that a lender cancelled a debt of $600 or more, which generally makes that amount taxable income to you. Receiving one often indicates the lender has treated the debt as cancelled for tax reporting purposes, but whether the debt is legally extinguished can depend on the specific facts and your state’s law. A 1099-C generally addresses the tax treatment of the debt. It doesn’t remove the lien. The form says nothing to the DMV, and it doesn’t instruct anyone to file a release. The DMV doesn’t even know the form exists.

Here’s the quick version of what actually changes at each stage:

| Event | Releases the Debt? | Releases the Lien on the Title? |

|---|---|---|

| Loan goes unpaid / delinquent | No | No |

| Lender charges off the loan internally | No — you may still legally owe it | No |

| Lender issues a 1099-C | Generally yes, for tax purposes | No — separate process |

| Lender sends a written lien release | N/A | Yes |

| State’s statutory lien-expiration rule applies | No | Sometimes, for older vehicles |

Rules vary by state — verify specifics at your local DMV or motor vehicle title division before acting.

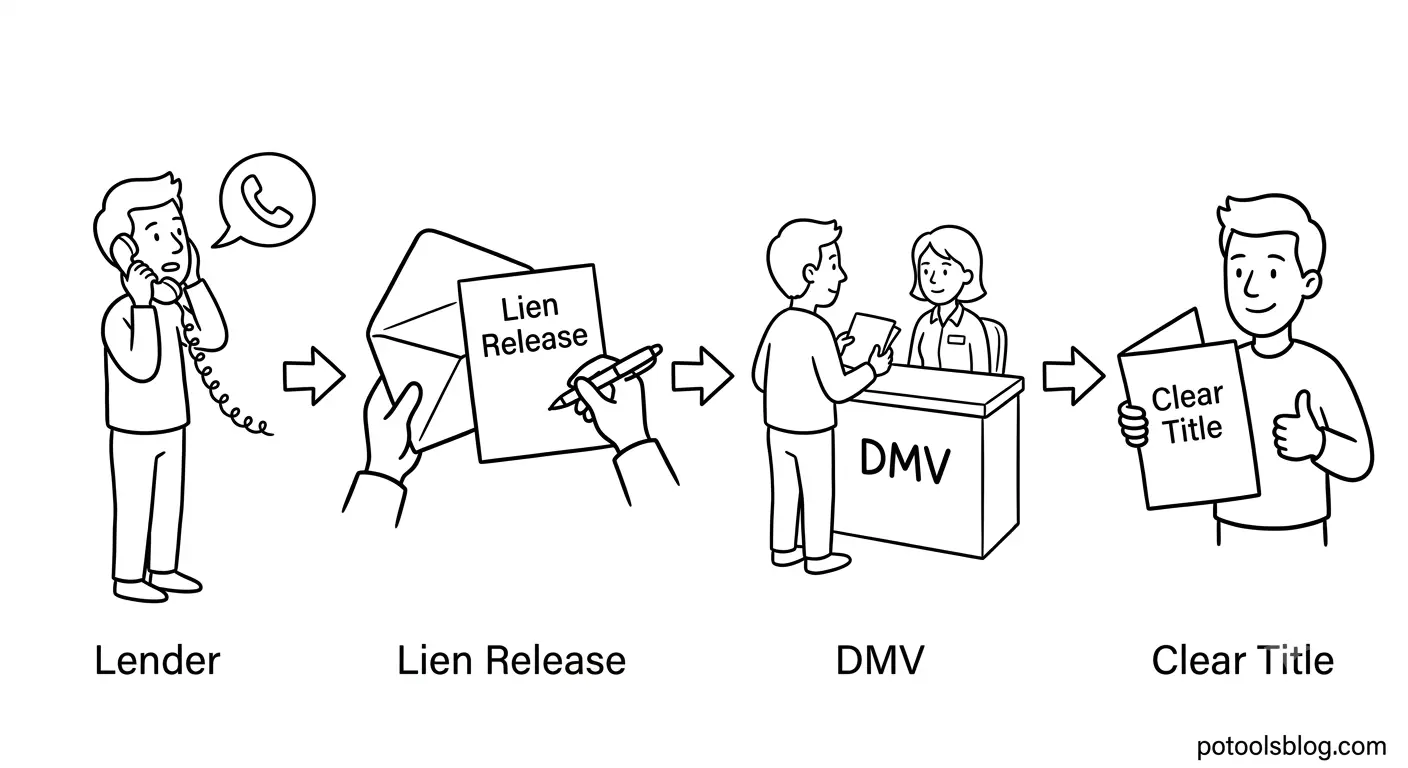

Getting the Lien Release: The Call Is Less Awkward Than You Think

Let’s address the anxiety first: calling a lender about a debt you defaulted on years ago sucks. Nobody wants to sit on hold to relive that. But here’s what actually happens on the other end — the rep pulls up a closed account and processes a paperwork request. That’s the whole interaction. Ask specifically for a lien release letter (some lenders call it a “lien satisfaction” or “release of security interest”). Reference the account number and, if you have it, the date the 1099-C was issued.

One wrinkle that trips people up after 7+ years: standard customer service sometimes can’t find anything. The account’s been purged from the active servicing system, and the rep on the general line will tell you exactly that. Don’t take it as a dead end — ask to be routed to the title department, loss mitigation, or asset recovery unit. Old, closed, or charged-off accounts usually still exist in one of those departments even after they’ve disappeared from the front-line system.

What to have ready before you call:

- Full name and any name that was on the original loan

- Vehicle Identification Number (VIN)

- Loan or account number, if you still have it

- The approximate date of the charge-off or 1099-C

Most lenders will mail or fax the release either to you or directly to your state’s DMV within a few weeks. If it stalls, ask for it in writing and follow up by mail. A paper trail matters if you need to escalate later.

One more thing worth doing while you wait: keep the car insured. It’s tempting to drop coverage on a car that isn’t running and isn’t going anywhere, but an uninsured vehicle sitting in a driveway can turn into its own problem — a code-compliance fine, a tow company hauling it off as abandoned, or a liability gap if anything happens to it before the paperwork clears. A basic liability policy is cheap insurance against a much bigger headache while the lien release is in progress.

Once You Have the Lien Release, Here’s What Comes Next

Take the release to your state’s DMV or motor vehicle title office and apply for a duplicate title in your name, with the lienholder removed. In ELT states, the lien can disappear from your record before you even apply.

Check for back registration or title fees before you go — this is the step that catches people off guard and turns a ten-minute counter visit into a second trip. A number of states won’t issue a clean title until unpaid annual registration is settled, even on a car that hasn’t moved in years.

Worth doing at this stage: run the VIN through the National Motor Vehicle Title Information System (NMVTIS), a federally supported database that shows whether a title’s been flagged salvage, junk, or otherwise marked. Check your vehicle’s title record at nmvtis.gov.

What If You Never Received the Title After Paying Off the Loan?

Different situation, same paperwork gap. Sometimes a loan gets paid off in full, but the lender never files the release — the account gets sold to a new servicer mid-payoff, the original lender merges or shuts down, or the paperwork just falls through the cracks on their end. Years later you’re holding a paid-off car with a title that still lists a lienholder who has no idea the loan is settled.

The process is nearly identical to a charged-off loan: request a lien release referencing your final payment date rather than a 1099-C, check the DMV’s ELT record first in case it’s already cleared, and fall back to a bonded title if the servicer can’t be located. The one difference — keep your payoff confirmation or final statement if you still have it. It’s not required everywhere, but it removes any question at the DMV counter.

Documents You’ll Probably Need

- Vehicle Identification Number (VIN)

- Government-issued ID

- Lien release letter (once obtained)

- 1099-C, if you received one

- Current or expired registration

- Old loan or account number

- Current address matching your ID

Having these ready before you call the lender or visit the DMV cuts out most of the back-and-forth.

What If the Lender Won’t Answer or Doesn’t Exist Anymore?

Old accounts get sold, merged, or the servicer just stops existing. There are still paths forward — they take more paperwork.

| Method | What It Requires | Typical Cost | Time Frame | Best For |

|---|---|---|---|---|

| Standard lien release | Lender sends release letter | Usually free | 2–6 weeks | Lender is responsive |

| Bonded title | Surety bond (often 1.5x vehicle value), DMV application | $75–$300+ for the bond | 2–4 weeks | Lender unresponsive but exists |

| Mechanic’s or storage lien | Vehicle left with a licensed shop or tow yard, unclaimed for a set period | Varies by state and shop | 30–90 days | Vehicle abandoned at a business |

| Statutory “stale lien” rule | Some states auto-expire liens on vehicles past a certain age | Free (DMV filing fee only) | Immediate once eligible | Older vehicles, long-charged-off loans |

| Non-repairable / salvage-only title | DMV affidavit confirming vehicle is scrap-only | Low DMV fee | 1–3 weeks | Vehicle has no resale value |

Costs, bond percentages, and eligibility ages vary significantly by state. Verify current rules at your state DMV before choosing a route.

A word of caution on the mechanic’s or storage lien route: this only applies when a licensed, third-party repair shop or tow yard legitimately performed work on or stored the vehicle and it went unclaimed. Filing a mechanic’s lien against your own car, or arranging one without a real shop and real diagnostic work behind it, can constitute title fraud in most states. If this route doesn’t reflect an actual, documented shop transaction, skip it and use the bonded title process instead.

If the bank goes radio silent, your best escape hatch is a bonded title. You buy a surety bond — essentially insurance for the DMV against a future ownership dispute — and the state issues a title backed by it. After a set period, commonly three to five years with no competing claim, it typically converts to a standard title, though conversion rules vary by state.

The stale-lien rule is the one almost nobody knows about. A number of states will drop a lien from an older vehicle’s title automatically once a set number of years have passed since it was filed — often somewhere in the 5-to-10-year range for vehicles over roughly a decade old. Check your state’s specific statute through the Consumer Financial Protection Bureau or your DMV before assuming it applies to you.

Most Junkyards Will Turn You Away Without This Document

Licensed scrap yards are generally required to verify ownership before accepting a vehicle — specifically because unverified scrapping is a common way stolen cars get destroyed for parts. A decade of dust on the hood doesn’t change their intake rules.

A non-repairable or salvage-only title, available through most state DMVs for vehicles with no resale value, exists for exactly this gap, and it’s usually quicker and cheaper to get than a standard duplicate title.

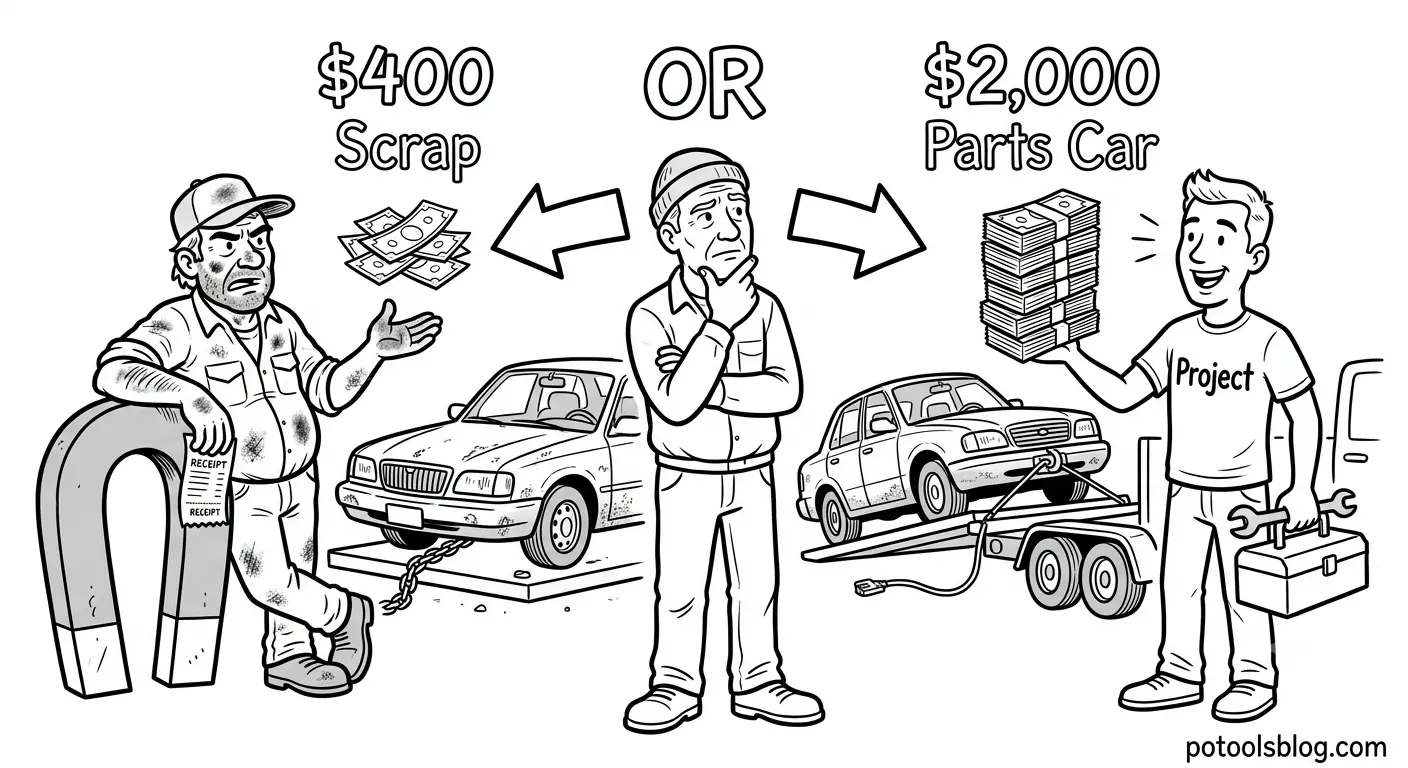

Before You Scrap It, Check Whether It’s Worth Selling Instead

A blown engine usually destroys the engine’s value — not the vehicle’s value. Everything else on the car might still be worth something:

- Transmission

- Interior

- Doors and body panels

- Wheels

- AWD or 4WD system

- ECU

- Airbags

- Glass

A car that’s been sitting in a garage rather than outside typically has minimal rust. Enthusiast models with bad engines routinely sell for $1,000–$3,000 as parts or project cars — a very different number than scrap-metal weight pricing, which tends to land closer to $300–$500 for the same vehicle.

Once you have clean title paperwork, three realistic options:

- Private sale as a parts or project car — usually the highest return, especially for models with an active enthusiast following.

- Junk car buying services — a quote and pickup within a day or two, typically for more than scrap-metal weight pricing.

- Donation to a registered charity — some accept vehicles without a title already in hand, and it converts the car into a tax deduction instead of cash.

The Tax Bill on Your 1099-C Might Be Reducible

This is the part most people never check. If your total debts exceeded your total assets at the moment the loan was cancelled, you may qualify for the insolvency exclusion under IRS rules, which lets you exclude some or all of the cancelled debt from taxable income.

The math: subtract your total liabilities from your total assets immediately before the cancellation. Say you had $45,000 in total debts and $38,000 in total assets — you were insolvent by $7,000. If your 1099-C showed $6,000 in cancelled debt, all of it could potentially be excluded, since the excluded amount can’t exceed your insolvency amount. You’d claim this on IRS Form 982, filed with your return for the tax year printed on the 1099-C — not the year you happen to be sorting out the title. If the cancellation was reported for 2021, the exclusion belongs on a 2021 return (or an amended one), even if you’re dealing with the DMV in 2026. Review Form 982 and its instructions at irs.gov.

If you already filed and paid tax on the cancelled debt without knowing about this, the exclusion doesn’t apply itself retroactively — you’d generally need to file an amended return, and a tax professional can confirm whether your numbers qualify and whether you’re still inside that window.

What to Actually Do, in Order

Check your title status online first — you might already be lien-free. If not, call the lender. While that’s processing, run an NMVTIS check so you know exactly what’s on record. If the lender goes quiet after a reasonable follow-up window, don’t wait indefinitely — move to a bonded title. A $150–$250 bond premium is a small cost against a car that’s likely worth $800–$3,000 or more for parts once you stop comparing it to scrap pricing. Scrapping should be the last option on the list, not the default — even a non-running garaged car this age usually clears well above scrap value in a private parts sale.

Frequently Asked Questions

Does a 1099-C mean I own the car free and clear? No. It only affects the tax treatment of the debt. The lien stays on the title until the lender sends a formal release or a state process removes it.

Can a lender repossess my car years after charging off the loan? In many states, yes, as long as the lien remains active — the charge-off and 1099-C don’t erase that right by themselves. It becomes less likely the longer the account has gone untouched, but “less likely” isn’t the same as “off the table.” Getting the lien formally released is what actually removes the risk.

How long does it take to get a duplicate title after a lien release? Most states process one within two to six weeks of receiving the release, though ELT states can be faster since the release may already show up in the DMV’s system.

What happens if the original lender no longer exists? Loans get sold or transferred to other servicers or debt buyers regularly. Start with an NMVTIS title check to see who’s currently listed as lienholder, then contact that company directly. If no lienholder can be identified at all, a bonded title is typically the path forward.

Is a bonded title as good as a regular title? For selling, scrapping, or registering the vehicle, functionally yes in most states. It carries a bond behind it for a set number of years in case a prior owner or lienholder later disputes it, after which it typically converts to standard — though the exact terms depend on your state.

Bottom Line

A charged-off loan and a 1099-C usually mean the lender has treated the debt as cancelled for tax reporting purposes. Neither one touches the lien. You still need a formal release and a duplicate title before you can legally sell or scrap the car. For most people, that’s one phone call, a DMV visit, and — if the lender goes quiet — a bonded title as the fallback that actually works. It’s a few weeks of paperwork against however many years that car has been sitting there. Once the title clears, getting it off your property is the easy part.

Disclaimer: The information on potoolsblog is for educational purposes only and does not constitute financial, tax, or legal advice. Always consult a qualified financial or legal professional before making decisions about your money or your vehicle’s title. Card terms, insurance rates, and government program rules are subject to change; verify current details with the issuer or relevant agency before acting.