Quick Answer

Yes — a check can still clear a day or two after your bank “freezes” your account. A freeze blocks new withdrawal requests going forward; it usually can’t pull back an item that another bank had already accepted and pushed into the interbank clearing system before the freeze took effect. If fraudulent checks or debits keep posting, the fix isn’t a tighter freeze — it’s coordinating with your bank to redirect your recurring payments to a new account, then closing the compromised one, and putting your fraud claim in writing so the legal clock on the investigation actually starts.

Fraudulent Checks Cleared After You Froze Your Bank Account? Here’s Exactly What’s Happening

You mailed checks, they never reached the people you sent them to, and your account is now bleeding money to strangers — even after a bank rep told you it was locked down.

That gap between “frozen” and “safe” is exactly where mail thieves operate, and it’s a bigger business than most people assume. Check fraud losses across the Americas totaled an estimated $21 billion in 2023, according to Nasdaq Verafin’s analysis of Bank Secrecy Act data, with roughly $1.3 billion of that landing directly on U.S. financial institutions. In just the six months after FinCEN’s 2023 alert on the topic, banks reported more than $688 million in suspicious activity tied specifically to mail-theft check fraud, across over 15,000 individual reports.

The rest of this guide walks through why the freeze didn’t stop everything, what to do in the next 24 hours, what happens after you file the claim, who’s actually on the hook for the loss, and how to keep it from happening again.

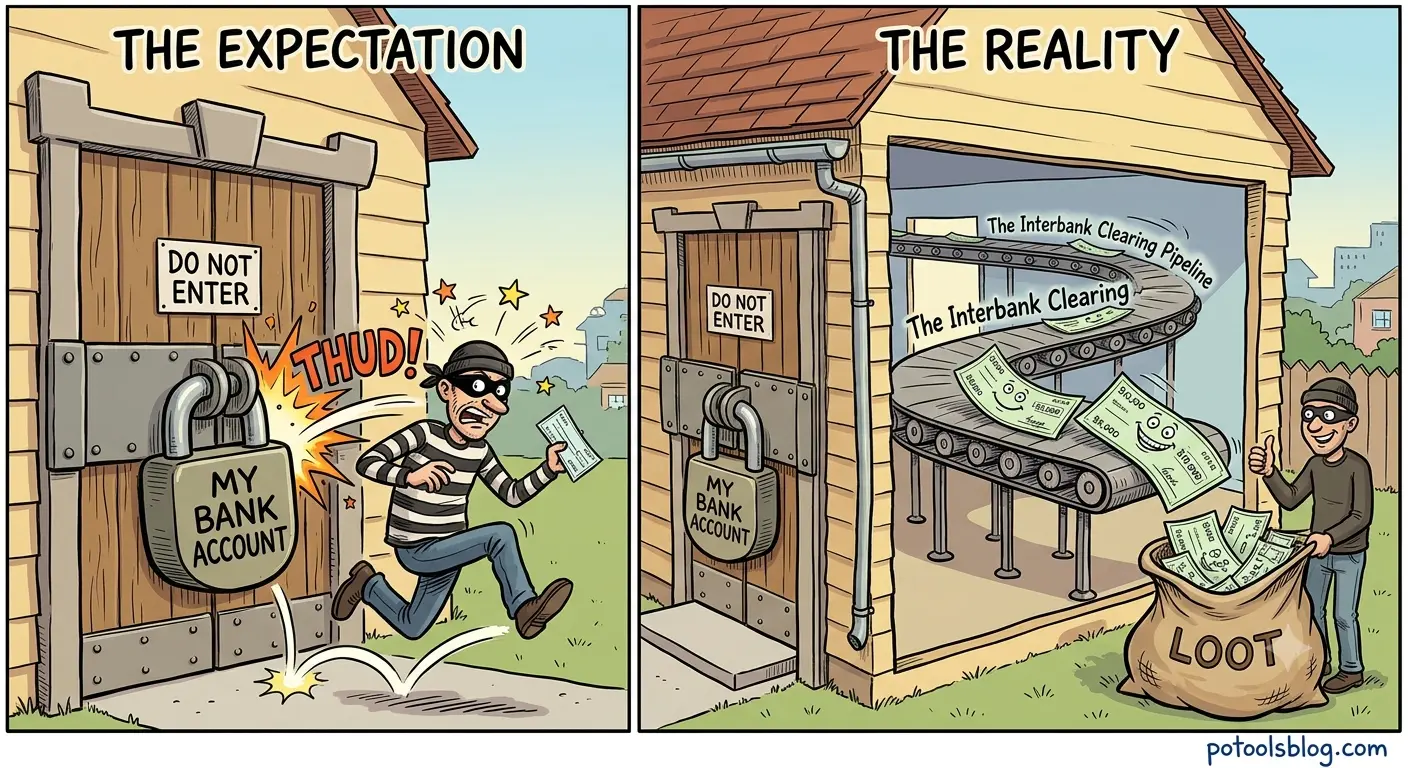

Why Did Fraudulent Checks Clear After My Bank Account Was Frozen?

A freeze is a front-door lock. It stops new transactions from being initiated or authorized against your account starting the moment it’s applied. What it doesn’t do is reach back into transactions that were already moving through the system before that moment.

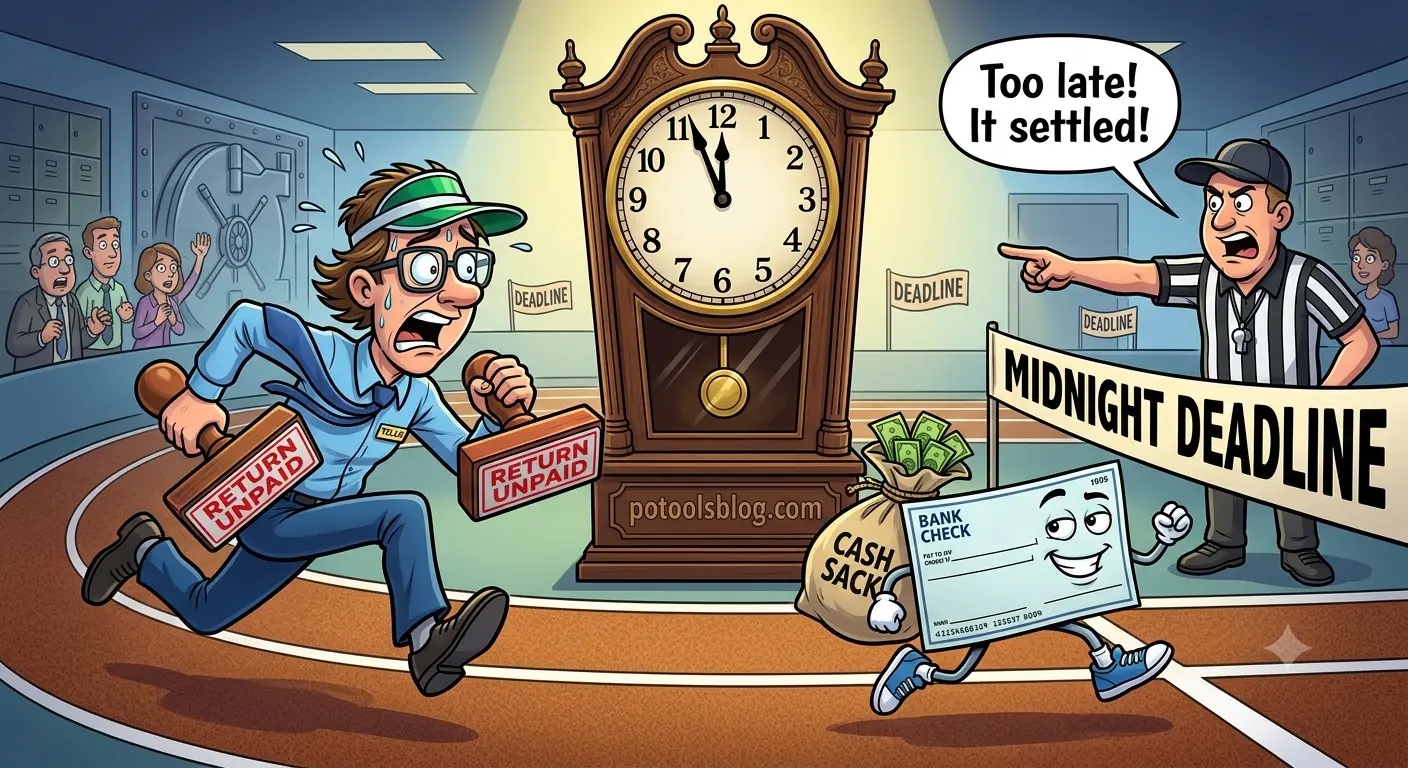

Here’s the mechanic banks rarely explain clearly: once a check is deposited at another bank, that bank presents it to yours for payment through the Federal Reserve or a private clearinghouse. Under UCC Section 4-302 — sometimes called the midnight deadline rule — your bank generally has until midnight of the next banking day after receiving that presented check to return it unpaid. Miss that window, and the bank becomes liable for the amount; the check is treated as paid. If a fraudulent check was already presented and sitting inside that settlement window when you called to report the fraud, a same-day freeze can be too late to intercept it — even though the money hadn’t visibly left your account yet.

That lines up with what banks tell customers in this exact situation: items already in the clearinghouse pipeline before a freeze was entered can still settle. It isn’t usually a sign your bank ignored you. It’s a sign the freeze arrived after the item had already crossed into a different part of the payment system.

How a Stolen Check Actually Moves

Check written & mailed

↓

Stolen from a mailbox, collection box, or via a compromised USPS arrow key

↓

Washed, "cooked," or deposited with a forged endorsement

↓

Deposited at another bank and presented for payment

↓

Enters the interbank clearing pipeline (governed by the UCC's midnight deadline rule)

↓

You discover the fraud and freeze your account → too late for items already in the pipeline

↓

You redirect autopay/deposits and close the account → stops the next item coldIs Freezing Your Account the Same as Closing It?

No, and the difference matters more than most people realize when checks were physically stolen.

| Account Freeze/Hold | Account Closure | |

|---|---|---|

| Blocks new transaction attempts | Yes | Yes |

| Stops items already in the clearing pipeline | Often no | Yes, going forward |

| New account/routing number issued | No — a thief may still have the old numbers | Yes |

| Direct deposits and autopay | Usually stay connected | Must be redirected before closing |

| Best for | Buying yourself a few hours to plan next steps | Neutralizing a stolen checkbook or compromised account number for good |

A stolen check doesn’t just expose one transaction — it exposes your full account number and routing number, printed right on the paper. Anyone holding that check can use those numbers to pull an ACH debit, not just cash the check itself. A freeze buys you time. It doesn’t erase the numbers a thief already has. For most consumers, closing the compromised account — once a replacement is in place — is what actually stops that.

What Should You Do Right Now If Stolen Checks Keep Clearing?

- Call your bank’s fraud department today and tell them you want a replacement account opened, not just a freeze on the current one.

- Redirect direct deposits and automatic payments to the new account first, so payroll, rent, and utility payments aren’t disrupted mid-transition.

- Close the compromised account once the replacement is active and transfers are confirmed — this cuts off anyone still holding your old account and routing numbers.

- Submit a written fraud affidavit for every transaction, listing check numbers, dates, and amounts. A verbal report alone often doesn’t start your bank’s formal investigation clock.

- File a police report. It rarely leads to an arrest, but nearly every bank, card issuer, and regulator treats it as required documentation for a bank fraud claim.

- Report the mail theft to the U.S. Postal Inspection Service at uspis.gov/report or 1-877-876-2455 — the federal agency that investigates crimes involving the mail.

- Request the fraudulent check images from your bank, including the forged signature or forged endorsement side, and keep copies with your claim file.

- Place a fraud alert or credit freeze with the credit bureaus and pull your reports at annualcreditreport.com, since a stolen check can expose your account number, address, and signature together.

- Follow up in person if the claim stalls. Fraud paperwork occasionally sits unprocessed in an internal queue; a branch visit and a direct request for a fraud-department supervisor is often what moves it.

What Happens After You File a Bank Fraud Claim?

Once your written claim is in, the process generally follows a predictable arc — though exact timing depends on your bank and on whether the disputed item was a paper check or an electronic pull.

- Day 1 — the claim is logged. Get a case number and note it; you’ll reference it in every follow-up.

- Within 10 business days — a decision on provisional credit. For anything covered by Regulation E, your bank must finish its investigation or issue provisional credit within this window if it needs more time.

- Up to 45 days — the investigation continues. Your bank may contact the depositary bank (the one that accepted the fraudulent deposit) for the original check image, endorsement, and account-opening details tied to where the money went.

- Final determination. If the item wasn’t properly payable, the provisional credit becomes permanent or a new credit is issued. If the claim is denied, the bank must explain why in writing, and you can request the documentation it relied on.

If a claim runs past that window with no explanation, that’s your cue to escalate — first to a branch manager or fraud supervisor, then to your bank’s federal regulator (see the reporting table below).

Two Different Frauds, Two Different Rulebooks

Something easy to miss: if thieves used your check’s printed account and routing number to pay their own credit card bill electronically, and also physically forged and cashed other checks, you’re dealing with two separate legal frameworks at once.

Electronic pulls — an ACH debit made using your account and routing numbers, even without a physical check — generally fall under the Electronic Fund Transfer Act and its implementing rule, Regulation E. You have 60 days from the statement date to report an unauthorized transfer; once you do, your bank has 10 business days to investigate (20 for accounts open less than 30 days). If it needs more time, it can take up to 45 days — but only if it provisionally credits your account for the disputed amount within that first 10-day window.

Physical checks that are forged, altered, or deposited with a forged endorsement are instead governed by state law adopted from the Uniform Commercial Code, not Reg E. There’s no uniform federal timeline here — but UCC Section 4-406 requires you to review statements and report unauthorized items with “reasonable promptness,” commonly treated as around 30 days, or you risk losing your reimbursement right for later items of the same type. Wait more than a year, and Section 4-406(f) bars the claim entirely regardless of who was at fault.

Knowing which framework applies to which transaction changes what you can reasonably expect and by when: Reg E gives you a hard federal deadline; the UCC path depends more on your state’s law and how quickly you reported it.

What Is Check Washing, and Why Is It Spiking Right Now?

Check washing is when a stolen check is treated with common solvents — acetone, bleach, or nail polish remover — to lift the handwritten payee name and dollar amount while leaving the pre-printed bank information intact. The check is then rewritten for a different payee or a larger amount. A newer variant, “check cooking,” skips the chemistry: thieves scan the check and use image-editing software and a decent printer to manufacture several altered or fully counterfeit checks from a single stolen original.

The supply chain feeding this has gotten more organized. USPS mail carriers carry a small number of master keys — called arrow keys — that each open dozens or hundreds of collection boxes and cluster mailboxes along a route. USPIS data reviewed by 11Alive News showed arrow key thefts rising 27% in 2024, with more than 3,400 keys reported stolen nationwide. A USPS Office of Inspector General follow-up audit released in May 2026 found that roughly 19% of arrow keys listed in the agency’s own tracking system were missing or unverifiable, and that more than 40% of keys recorded as lost or stolen were never formally reported to postal inspectors.

The broader BSA data backs up the trend: SAR filings tied to check fraud rose from around 350,000 in 2021 to roughly 680,000 in 2022 — nearly doubling — and have stayed near that level since, with an estimated 682,000 check-fraud SARs filed in 2024. Separately, USPIS logged 299,020 mail theft complaints between March 2020 and February 2021, a 161% jump from the year before, and USPS recorded 38,500 high-volume mail-theft incidents from October 2021 to October 2022, with more than 25,000 in just the first half of 2023.

None of that is a reason to panic about every check you’ve ever mailed. It’s a reason to treat a blue collection box outside a post office as meaningfully less secure than the slot inside the building — especially around a holiday closure, when mail sits longer before pickup.

Will Your Bank Reimburse You for Forged or Altered Checks?

In most cases, yes — but it’s not automatic and it’s not unconditional.

Under UCC Section 4-401, a bank may only charge your account for items that are “properly payable,” meaning you actually authorized them. When a bank pays a forged or altered check, that payment generally isn’t properly payable, and the bank’s default duty is to make you whole — treated as a contractual obligation, not something that hinges on proving the bank was careless. A 2018 update to Regulation CC reinforced this with a presumption of liability: the bank that first accepted the deposit is presumed responsible for an altered check, while your own bank (the paying bank) is presumed responsible for a forged or counterfeit one.

The main way banks push back is by arguing you failed to exercise “ordinary care” in a way that substantially contributed to the fraud — for example, leaving blank checks somewhere obviously insecure. Courts have generally set a high bar for that defense. A customer who reports promptly, wasn’t involved in the theft, and didn’t benefit from it is usually still made whole even when the fraud itself was sophisticated. The practical lesson isn’t that you’re at fault for mail theft you had no way to prevent. It’s that reporting quickly, and in writing, protects a reimbursement right you already have.

Who Do You Report Stolen Checks and Mail Theft To?

| Where | Why |

|---|---|

| Your bank’s fraud department (in writing) | Starts the formal investigation and reimbursement clock |

| Local police department | Produces the police report almost every bank and regulator will ask for |

| U.S. Postal Inspection Service — uspis.gov/report | Federal agency that investigates mail theft specifically |

| FBI Internet Crime Complaint Center — ic3.gov | Feeds national fraud-pattern data used to track organized theft rings |

| CFPB complaint portal — consumerfinance.gov/complaint | Escalation path if your bank is slow-walking or denying a legitimate claim |

| OCC — helpwithmybank.gov | Regulator for nationally chartered banks specifically |

| NCUA — ncua.gov | Regulator for federally chartered credit unions |

| FTC — identitytheft.gov | Recovery plan if the stolen check exposed enough data for identity theft |

FinCEN’s own alerts on this exact problem — the 2023 nationwide surge alert and its follow-up trend analysis — are also worth skimming if you want the primary source behind the statistics above.

How Do You Stop This From Happening Again?

- Drop outgoing checks inside the post office, in the lobby slot or at the counter, rather than in a freestanding collection box — especially right before a holiday closure, when mail sits longer before the next pickup.

- Use a genuinely indelible gel pen. Not every pen marketed as check-safe actually resists solvents; look for ink certified to ISO 12757-2 rather than a generic “security pen” label.

- Enroll in USPS Informed Delivery for a daily image preview of what’s arriving, so a missing item stands out faster than a monthly statement would show it.

- Ask about Positive Pay if your bank offers it. It matches every check presented against a list you’ve pre-approved and flags anything that doesn’t match before it pays — a counterfeit-check safeguard that a freeze can’t replicate.

- Move recurring payments to electronic bill pay or ACH where the payee accepts it, since there’s nothing printed for a thief to steal.

- Check your account more often than every 7–10 days for a few weeks after mailing anything with your account number on it.

What We Would Do

For a personal account already showing fraudulent checks or debits, we’d move fast on sequencing, not just on urgency: coordinate with the bank the same day to open a replacement account, redirect direct deposits and automatic payments as soon as the new account is active, and then close the compromised account — rather than leaving it open behind a freeze indefinitely.

We’d also submit the fraud affidavit in writing immediately, even if a phone rep says it’s “already noted.” A written notice is what starts the clock on the UCC’s reasonable-promptness standard and, for anything pulled electronically, Regulation E’s 10-business-day investigation window. On a case involving both a forged check and a pending second item, waiting a few extra days to formalize the claim adds risk for very little upside.

The one real exception: a business account with high check volume may be better served by enrolling in Positive Pay and tightening internal controls rather than closing and re-issuing hundreds of outstanding vendor checks. For a personal account, the close-after-redirect sequence above is almost always the cleaner move.

Frequently Asked Questions

Can a check still clear after my bank freezes my account? Yes. A freeze blocks new authorizations going forward, but a check already accepted by another bank and presented for payment can still settle under the UCC’s midnight deadline rule before your bank is able to intercept it.

Should I freeze my account or close it after check fraud? For most consumers, closing the compromised account — after coordinating with the bank to redirect payroll and automatic payments to a new one first — is safer than relying on a freeze alone. A freeze doesn’t change the account and routing numbers already exposed on a stolen check; closing it does.

Will my bank reimburse me for forged or altered checks? Usually, yes. Under the UCC, banks generally bear the loss for checks that weren’t properly authorized, as long as you report the fraud with reasonable promptness — commonly understood as within about 30 days of the statement showing the item.

Do I actually need a police report? In almost every case, yes. It rarely results in a fraudster being caught, but banks, card issuers, and regulators typically require it before they’ll formally process a fraud claim.

Is it still safe to mail paper checks? It’s riskier than it used to be. Mail theft-related check fraud has climbed sharply in recent years, driven in part by stolen USPS master keys. Dropping checks inside the post office and shifting recurring payments to electronic transfers where possible meaningfully lowers your exposure.

Where This Leaves You

A frozen account stopping every dollar the moment you call is a reasonable assumption — it’s just not how the check-clearing system works. Once you understand that timing gap, the response is straightforward: redirect your recurring payments to a new account, close the compromised one, and put your fraud report in writing while looping in USPIS alongside your bank. The main exception is a business juggling a large volume of outstanding checks, where Positive Pay may be the better first move instead of an immediate closure.

Disclaimer: The information on Potoolsblog.com is for educational purposes only and does not constitute financial or legal advice. Always consult a qualified financial or legal professional before making decisions about your money. Bank policies, regulatory timelines, and state laws referenced here are subject to change; verify current details with your financial institution or the relevant agency before acting.