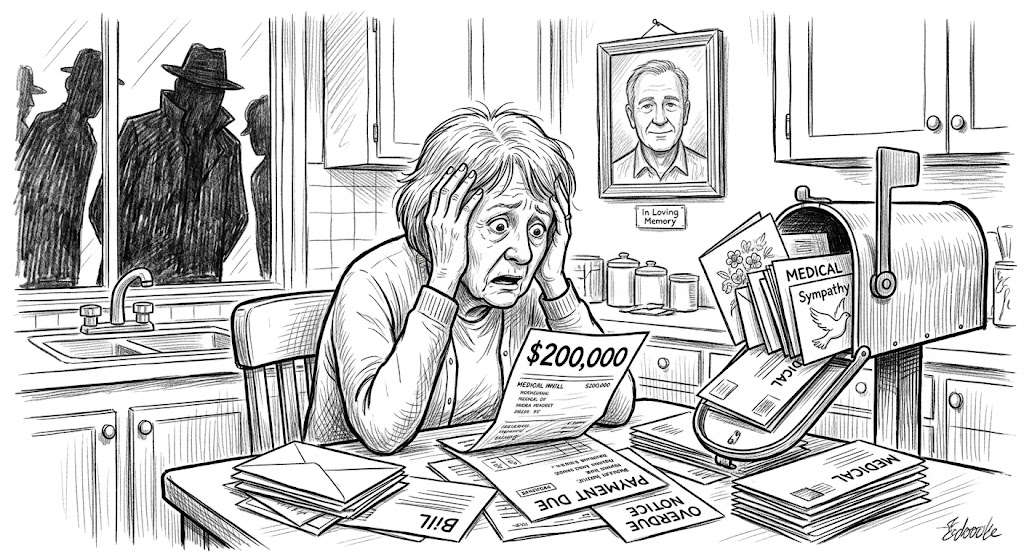

Just Imagine, You are sitting at your kitchen table, the silence in the house is heavy and unfamiliar. It’s only been a few weeks since you lost your spouse. You’re barely doing your own work, remembering to eat only because a neighbour dropped off a casserole. You walk out to the mailbox, hoping for a kind sympathy card, but instead, you pull out an envelope with a sterile, windowed front. Inside is a bill from the hospital. The total at the bottom looks like a phone number: $200,000.

Your stomach instantly drops, and the terrifying question hits you: Is a surviving spouse responsible for medical bills after death? The short answer is a classic legal tease: it depends entirely on where you live and what paperwork you signed. But before you panic-pay a single dime of your own hard-earned cash, you need to understand that debt collectors deeply bank on your grief, your fear, and your confusion.

While children rarely inherit a parent’s debt, the rules change drastically for husbands and wives. Let’s look at how the law actually protects you, and where the hidden traps lie.

Your Geography Dictates Your Financial Liability

When a person passes away, their bills don’t automatically transfer to their family. Instead, they attach to a fresh legal entity known as “the estate.” Think of the estate like a temporary corporation that holds everything the deceased person owned.

If you are a grieving adult child, you can almost always tell the hospital to go kick rocks. But if you are a surviving spouse, the very first question a judge will ask is: Where did you live?

The Common Law Shield (The Majority)

If you live in a common law state (like Virginia, Pennsylvania, New York, or Ohio), the law treats your financial identity as completely separate from your spouse’s. If the medical bill has only their name on it, it is their debt alone.

The hospital must line up like any other creditor to collect from your partner’s solo estate. If your partner died with zero assets held in their name alone—meaning everything you owned was joint with rights of survivorship (WROS)—the estate is effectively broke. And when an estate is broke, creditors are simply out of luck. They cannot legally touch your personal paycheck, your solo bank accounts, or your joint home.

The Community Property Trap (The Dynamic Shifts)

If you live in a community property state, the financial shield vanishes. These states view marriage as a single economic team. Anything bought, earned, or borrowed during the marriage belongs 50/50 to both parties.

In these regions, asking do you have to pay medical bills after someone dies swings violently toward yes. Because healthcare is considered a debt incurred to sustain the household during the marriage, a debt collector can legally sue you, target your joint marital property, and attempt to garnish your personal salary—even if you never signed a single hospital form.

| Community Property States (Watch Out) | Common Law States (Shields Up) |

| Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, Wisconsin | Virginia, Pennsylvania, New York, Ohio, Maryland, Illinois, and 35 others |

The Centuries-Old Legal Loophole Hospitals Love to Use

“Hold on,” you might say. “I live in New Jersey, which is a protective common law state. The hospital is still threatening to sue me!”

Welcome to one of the oldest, sneakiest legal loopholes in America: The Doctrine of Necessaries (sometimes called the Statute of Family Expenses). This is a centuries-old rule left over from English common law. It dictates that married couples have a legal obligation to provide the basic necessities of life—food, shelter, and medical care—to one another.

In states that still uphold this doctrine (like New Jersey, North Carolina, and Illinois), a hospital can argue that because they treated your spouse, you are on the hook for the bill if your spouse’s estate cannot pay.

The Insight: Debt collectors love to throw this term around to terrify widows. However, in many states, courts require the hospital to aggressively exhaust every single penny of the deceased spouse’s estate first before they can look at you. If a collector calls using this terminology, do not agree to anything until you speak with a local consumer protection attorney.

The Blurry Midnight Signature That Changes Everything

Let’s look at the absolute worst-case scenario. You live in a protective common law state. Your spouse had no assets, so the estate is empty. Yet, the debt collector has a piece of paper that legally forces you to pay. How?

Because of the midnight admission paperwork chaos.

When your spouse was rushed into the Emergency Room, a stack of forms was pushed across the desk. Your eyes were blurry with tears, your heart was hammering, and the receptionist said, “We just need you to sign here so we can treat them.” You signed. But what did you sign?

[ ] AUTHORIZED REPRESENTATIVE (Safe): You signed on behalf of your spouse because they were incapacitated. You have NO personal financial liability.

[X] GUARANTOR / RESPONSIBLE PARTY (Danger Zone): You signed a personal contract promising that if insurance defaults or leaves a balance, YOU will pay out of your own pocket.

If you signed as a guarantor, you bypassed the protections of state law and voluntarily entered a binding contract. If a collection agency claims you signed this, your very first move should be a cold, firm demand: “Send me the original intake form with my signature on it.” If they can’t produce it, they have no case.

So How to Handle Aggressive Collectors

If you are currently getting hounded for a massive medical balance and wondering do you have to pay medical bills after someone dies, treat debt collectors like aggressive stray dogs: don’t show fear, don’t run, and definitely don’t feed them.

Financial and Legal Disclaimer

Disclaimer: The information provided in this article does not, and is not intended to, constitute legal or financial advice; instead, all information, content, and materials available here are for general informational purposes only. Laws surrounding medical debt, probate, and spousal liability vary drastically by state and change frequently. Readers should contact a qualified estate planning or consumer rights attorney in their specific jurisdiction to obtain advice with respect to any particular legal matter or debt collection dispute.