You know what nobody talks about at the wedding?

The checking account.

You spend months planning flowers, seating charts, and the perfect first dance song. Then you come home from the honeymoon, look at two separate bank accounts and one shared Netflix password, and suddenly realize — nobody actually told us how to do this part.

Here’s the thing: the money question in marriage is not “joint account or separate accounts?” That debate is a distraction. Couples who fight about money aren’t fighting about accounts. They’re fighting about communication, trust, spending habits, and feeling like an equal partner.

The account structure is just furniture. You can rearrange the furniture all you want. If the foundation of the house is cracked, the couch placement doesn’t matter.

So let’s talk about what actually works — and what quietly destroys marriages that look perfectly fine on the outside.

The Real Question Isn’t “Joint or Separate” — It’s This

Here’s a thought experiment. Imagine two couples:

Couple A has one joint account. Every dollar goes in together, every bill comes out together. But one spouse makes most of the big spending decisions and the other feels like they need permission to buy a $40 sweater. They rarely discuss long-term goals. When a surprise expense hits, blame follows.

Couple B keeps separate accounts. Each pays an agreed-upon share into a shared pool for bills and savings. The rest is their own. They talk about money weekly — not dramatically, just practically, like two adults running a business together. There’s no scoreboard. There’s no resentment.

Which couple do you think fights more about money?

Research backs this up. According to a study published in the Journal of Consumer Research, how couples talk about money matters far more than how they structure their accounts. Couples who discuss financial decisions openly — regardless of their account setup — consistently report higher relationship satisfaction and fewer money-related conflicts. (Source: Journal of Consumer Research)

The account is a tool. Communication is the skill.

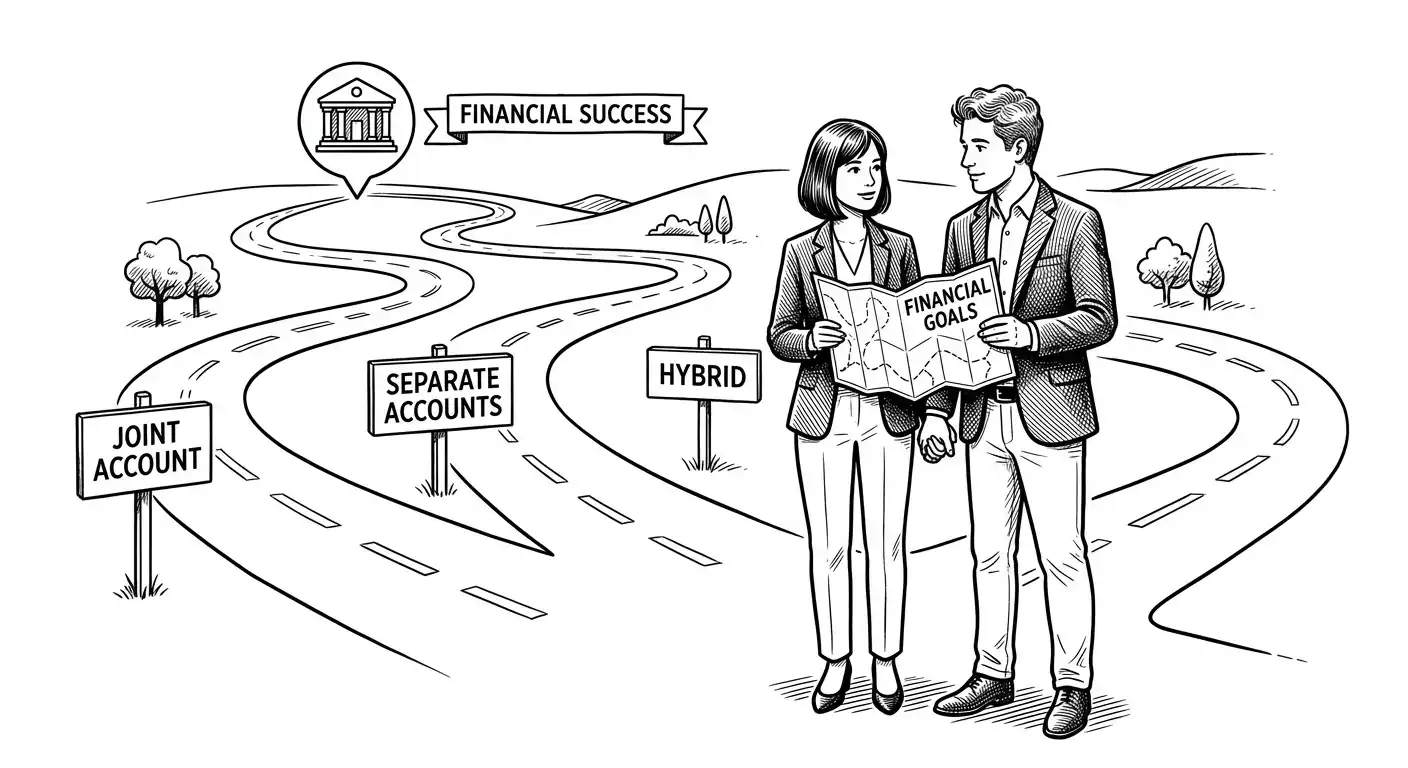

Married Couples Finances: Why the “One Right Way” Myth Is Costing You

Every financial advice column has an opinion. “Combine everything — you’re a team!” “Keep separate accounts — protect yourself!”

Here’s the truth most of those articles skip: what works depends entirely on you, your spouse, your income gap, your spending personalities, and your relationship history.

There is no universal answer. But there are universal principles.

Let’s break down the most common approaches, what they actually look like in practice, and who they tend to work best for.

The Three Main Systems Couples Use (And What They Don’t Tell You)

System 1: Fully Combined — One Account for Everything

Everything goes in together. Bills, savings, spending money, date nights — all from one pool. Most couples who do this say it forces a level of honesty and teamwork they value deeply.

What it looks like: Paychecks deposit into one joint account. A budget covers all expenses. Big purchases get discussed. Smaller purchases don’t require a committee meeting.

Who it works best for: Couples with similar spending habits, comparable incomes, and a high level of trust and communication. Couples who married young with minimal pre-existing assets. Couples who genuinely want full financial transparency as a way of building intimacy.

The catch nobody mentions: If one partner is a natural spender and the other is a saver, this system can breed resentment fast. The saver feels anxious watching the balance shrink. The spender feels judged every time they buy something “for themselves.” Without a structured budget and explicit “fun money” allowances, a fully combined account can make both people feel like they’re living in a financial fishbowl.

Fix it with: A clear monthly budget that includes a personal spending category for each person — no questions asked, no receipts required. Even $100/month in personal freedom can dramatically reduce money friction.

System 2: Fully Separate — Each Person Handles Their Own

Each spouse keeps their own account. Bills are split — either 50/50 or proportionally by income. Shared expenses get Venmo’d or handled by whoever’s turn it is.

What it looks like: “I pay the mortgage, she pays utilities and groceries.” Or: “We split everything by percentage of income.” Some couples who’ve been together for decades — particularly those who married later in life with established careers and assets — swear by this method.

Who it works best for: High earners with significant pre-marital assets. Couples in second marriages where each partner has existing financial obligations (kids from prior relationships, for instance). Couples with very different spending styles who’ve found peace in keeping their money lanes separate.

The catch nobody mentions: Fully separate finances require more communication, not less, because you have to negotiate every shared expense. Without intentional conversations about savings goals, retirement, and big purchases, couples can drift into separate financial lives — which can quietly erode the feeling of being a team.

Fix it with: A monthly “money date” — even 20 minutes over dinner — where you talk about shared goals, upcoming expenses, and where you both stand. The Financial Therapy Association has great resources on how couples can develop these habits without the conversation turning into a fight.

System 3: The Hybrid — Personal Accounts Plus a Joint Pool

This is what a growing number of financial experts recommend, and anecdotally it’s the system most couples land on after trial and error.

What it looks like: Both spouses keep their individual accounts from before marriage. They open a joint account (or designate one as joint). Each month, an agreed-upon amount flows into the joint account to cover shared expenses — mortgage, utilities, groceries, savings goals, vacations. Whatever’s left in each personal account is yours to use however you want. No explanation required.

Who it works best for: Almost everyone, honestly. Dual-income couples. Couples with an income gap. Couples who married later. Couples who just want some personal financial breathing room without compromising shared goals.

Why it works: It treats both partners as financial equals. It keeps shared goals funded. And it gives each person a guilt-free zone for personal spending — the $80 pedicure, the concert tickets, the weird kitchen gadget nobody asked for.

The catch nobody mentions: You have to actually agree on how much goes into the joint account — and revisit it as incomes change. And “personal” money needs to stay truly personal; if one partner is quietly building significant wealth while the other funds everything jointly, the system gets lopsided fast.

Joint Account vs. Separate Accounts: The Honest Comparison

| Fully Joint | Fully Separate | Hybrid | |

|---|---|---|---|

| Budget visibility | High | Low | Medium-High |

| Spending freedom | Low without structure | High | High |

| Simplicity | High | Low (lots of splitting) | Medium |

| Works if incomes differ | Depends | Harder | Yes |

| Protects you in crisis | No | Yes | Partially |

| Requires communication | Moderate | High | Moderate |

The Income Gap Problem Nobody Wants to Talk About

Here’s where couples get into real trouble: when one partner earns significantly more than the other.

A 50/50 split sounds fair on paper. In practice, if one spouse earns $90,000 and the other earns $40,000, splitting rent and groceries equally means the lower earner is stretching much harder. Over time, that math breeds quiet resentment — and sometimes financial dependency that feels like control.

The proportional contribution model solves this cleanly. Each person contributes the same percentage of their income to the joint account, not the same dollar amount. If the joint account needs $4,000/month and you earn 60% of household income, you contribute $2,400. Your spouse contributes $1,600. You both feel the same proportional weight. Neither is carrying the other.

According to research from Pew Research Center, about 29% of married couples now have roughly equal incomes — but the majority still have some gap. A proportional system acknowledges reality without making either partner feel inferior.

Shared Finances in Marriage: What the Research Actually Says

A widely cited acedemic research from the University of Michigan found that couples who pool all of their money together report higher relationship satisfaction than those who keep finances separate. The researchers theorized this is because full pooling creates a stronger psychological sense of partnership and shared fate.

But here’s the nuance: the benefit isn’t from the joint account itself. It’s from the shared financial identity — the sense of “we’re in this together.” Couples who achieved that feeling with hybrid systems or fully separate accounts (with good communication) showed similar satisfaction levels.

The account is a symbol. What you actually need is the mindset.

For a deeper dive, the Consumer Financial Protection Bureau (CFPB) has published practical guides on how couples can build shared financial goals regardless of account structure.

The Emergency Access Problem (And Why It Matters More Than You Think)

Here’s a scenario most couples never plan for until it’s too late.

Your spouse is hospitalized unexpectedly. Or worse.

If all the money is in an account solely in their name, you might not be able to access it immediately — even as their legal spouse, even in a crisis. Estate laws vary by state, and the probate process can take weeks or months. (Source: AARP on joint vs. separate accounts)

This is the one universal recommendation across almost every financial advisor, attorney, and estate planner: at minimum, make sure you each have your name on at least one account with enough to cover 2-3 months of household expenses. Whether that’s a joint account or an individual account with right of survivorship — it doesn’t matter. What matters is access.

If you’re keeping separate accounts, look into:

- Payable on Death (POD) designations — lets you name a beneficiary who receives the funds automatically, outside of probate

- Right of Survivorship — for joint accounts, the surviving spouse automatically inherits the balance

- Durable Power of Attorney — legal document that lets your spouse manage your finances if you’re incapacitated

These aren’t morbid preparations. They’re basic adult infrastructure.

Separate Bank Accounts After Marriage: The Hidden Protection Argument

There’s a conversation happening in personal finance spaces that doesn’t get enough mainstream coverage: financial safety within marriage.

The National Domestic Violence Hotline reports that financial abuse occurs in 99% of domestic violence situations — and it almost always involves one partner losing access to, or control over, money. Financial abuse can include denying access to funds, monitoring every purchase, demanding receipts, or outright stealing from a partner’s account.

This isn’t about assuming your spouse is dangerous. Most aren’t. But it is a reason why financial autonomy — having at least some money that is yours, accessible only to you — is a legitimate protective measure that experts openly recommend. Even in healthy marriages.

Financial therapists often suggest that each spouse should have at minimum:

- Their own individual account with a small emergency reserve

- At least one credit card in their own name (not just as an authorized user)

- Basic visibility into all household accounts and investments

This isn’t distrust. It’s financial literacy. And frankly, it protects both of you.

How Married Couples Manage Money Successfully: 5 Non-Negotiables

After stripping away everything else, here’s what the research, financial experts, and real-world experience agree on:

1. Talk about money before you need to. Don’t wait for a crisis to have a budget conversation. Schedule a monthly check-in — call it a “money date” if that helps — where you review what came in, what went out, and what’s coming up. Keep it low-stakes. Keep it regular.

2. Define what “fair” means for your household. Fair doesn’t always mean equal. Agree explicitly on who pays what, how shared costs are split, and how much personal spending each person is entitled to without needing approval. Put it in writing if that helps. Revisit it annually.

3. Set shared goals — in writing. Retirement savings. Homeownership. A vacation fund. A college fund. Shared financial goals give your money a direction. Without them, spending feels zero-sum — every dollar one person spends feels like a dollar the other person lost.

4. Eliminate financial secrecy. This is the big one. Secret accounts, hidden debt, undisclosed spending — these are rarely just financial problems. They’re relationship problems wearing a financial costume. Full financial transparency doesn’t mean joint accounts; it means no hiding. Both partners should have complete visibility into the household’s total financial picture.

5. Keep some autonomy — for both of you. Every adult deserves a zone of personal financial freedom. Even $50/month that’s truly yours — no explanation, no judgment — changes how people feel about money in a marriage. It’s not about distrust. It’s about dignity.

What About Credit Scores? Does Adding Your Name to Their Account Help?

This is a common question, and the answer is more nuanced than most people realize.

Bank accounts (checking and savings) do not appear on your credit report and do not affect your credit score. Period. Unless an account goes into default/collections. Closing a 15-year-old savings account? No credit impact. Opening a new joint checking? No credit impact.

What does affect credit scores:

- Credit cards (payment history, utilization, account age)

- Loans (auto, mortgage, personal)

- Hard inquiries when applying for new credit

If you’re added as an authorized user on your spouse’s credit card, that card’s history can appear on your report — for better or worse. If their card has great payment history, it can boost your score. If they’ve missed payments, it can hurt you.

If you want to build credit as a couple, the smartest move is usually:

- Each spouse maintains at least one credit card in their own name

- Keep utilization below 30% on all cards

- Pay balances in full each month

For a full breakdown of how marriage affects credit, Experian’s guide on marriage and credit scores is one of the most accurate and up-to-date resources available.

It’s Not the Account — It’s the Conversation

You can have joint accounts and fight about money constantly. You can have completely separate accounts and run a harmonious household with shared goals and zero resentment. And you can have the hybrid setup and coast through decades of marriage without a single money argument.

The account structure is not the variable. You are the variable. Your willingness to talk honestly. Your commitment to treating your partner as a financial equal. Your ability to separate “this is our money problem” from “this is your money problem.”

The couples who manage money well without conflict aren’t doing something exotic. They’re doing something boring and consistent: they talk, they budget, they show each other the numbers, and they give each other enough breathing room to feel like individuals, not just contributors to a shared fund.

Pick the system that fits your life. Then build the habits that make it work.

That’s the whole answer.

Quick-Reference: Resources for Married Couples Managing Money

- Consumer Financial Protection Bureau — Money Conversations for Couples

- Financial Therapy Association — Find a Therapist

- Pew Research Center — Dual Income Couples 2023

- Experian — Does Marriage Affect Your Credit Score?

- The Hotline — Understanding Financial Abuse

- AARP — Financial Steps After a Spouse Dies

This article is for informational purposes only and does not constitute financial or legal advice. For personalized guidance, consult a certified financial planner (CFP) or financial therapist.