When is an emergency fund “enough”? There comes a point in almost every saver’s life when this exact question stops being about math and starts being about survival. It’s the moment where the numbers on your screen say you are perfectly safe, but the persistent pit in your stomach completely refuses to go away.

Picture a couple in their early forties. They have followed every single piece of classic personal finance advice to the letter. Their retirement accounts are growing steadily, college savings for the kids are fully funded, and their mortgage is practically history. Their only remaining debt is a tiny car loan that’s about to be wiped out.

By every objective metric, they are winning.

Yet, when they log into their banking app at 2:00 AM and stare at their high-yield savings account, they don’t feel accomplished. They feel completely exposed.

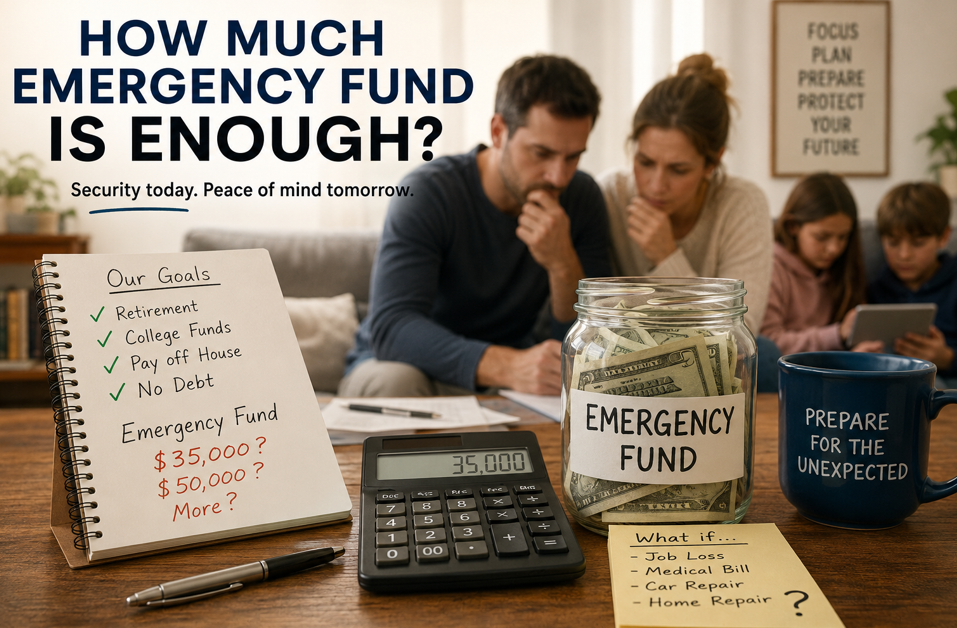

A $15,000 cash cushion used to feel like a fortune. Then it grew to $20,000. Then $30,000. Right now, they are sitting on $35,000, but the finish line just keeps moving. The question isn’t whether they are responsible—they clearly are. The real question is the psychological monster nobody wants to talk about: If $35,000 doesn’t buy you peace of mind, will $50,000? And if $50,000 still leaves you feeling vulnerable, what exactly are you trying to cure?

When a Financial Safety Net Becomes an Emotional Cage

When you first start scraping together cash, the goal is purely transactional. You need enough liquid cash to survive basic adulthood jump-scares: a medical bill, a sudden job loss, or a high insurance deductible.

But as your net worth grows, something weird happens. The emergency fund stops being a practical financial tool and starts acting as an emotional shield against the world.

That is where things get messy. Financial problems have hard numbers, but emotional trauma doesn’t.

A broken transmission costs exactly $5,000.

A new roof costs exactly $15,000.

Deep-seated fear and infinite “what-if” scenarios? That equation has no ceiling.

A broken appliance is a measurable risk. Fear isn’t. Fear doesn’t care if your account balance is $10,000 or $100,000. It just stands over your shoulder and whispers: “But what if a historic depression hits tomorrow?”

Why the Standard “3 to 6 Months” Rule Is Gaslighting You

If you ask any traditional financial advisor exactly how to calculate your safety net, you will get the exact same generic, copy-pasted advice: keep three to six months of living expenses tucked away.

The problem? Real life doesn’t care about clean, monthly intervals on a spreadsheet. Real life hits you with everything it’s got, all at once.

Imagine this perfectly plausible, devastating sequence: Your central air conditioning dies in the dead heat of July. Two months later, your car throws a rod on the highway. Three months after that, your company announces corporate restructuring and hands you a severance package.

Savers aren’t hoarding cash because they are crazy. They are doing it because they’ve watched the price of everyday life explode. A major home repair doesn’t cost a couple of grand anymore; it rivals the price of a decent used vehicle. Medical deductibles look like misprints, and a routine trip to the mechanic easily turns into a four-digit hostage situation. The world got wildly expensive, and our financial anxiety simply adjusted its targets to match.

The Summer of a Thousand Paper Cuts

We like to think of emergencies as massive, cinematic events—a catastrophic natural disaster or a dramatic corporate layoff. In reality, your savings are usually bled dry by a dozen completely boring, unglamorous problems.

The water heater floods the basement. The refrigerator stops cooling. The family dog eats a stray sock and ends up at an emergency vet clinic at 11:00 PM on a Saturday. None of these events will ever make the evening news, but together, they can vaporize $20,000 before you even have time to process the shock.

People aren’t always saving for the end of the world. Most of the time, they are just deeply traumatized by that one insanely expensive year where every single piece of property they owned broke down at the exact same time.

What Crisis Are You Actually Solving?

To break out of the loop of moving your savings goals, you have to ask the one question personal finance articles completely ignore: Enough for what?

Without defining the exact scenario you are terrified of, you are trying to solve an algebraic equation without knowing the variables. Your specific life situation completely changes your survival number:

-

The Job Security Factor: A tenured government worker with rock-solid employment needs a completely different cash cushion than a freelance consultant whose income can drop to zero the second a major client cuts a contract.

-

The Housing Dynamic: A renter can simply call a landlord when the plumbing goes sideways; a homeowner has to whip out a credit card and deal with the contractor directly.

-

The Income Stream: A dual-income household has a built-in safety valve if one spouse gets laid off. A single-income family is walking a tightrope without a net.

Why the Paid-Off House Changes the Whole Game

We constantly forget how much consumer debt and heavy liabilities distort our relationship with money. When your mortgage is entirely gone and your vehicles are paid off, your absolute baseline expenses drop off a cliff.

Losing your job becomes a massive annoyance, not a fast track to foreclosure. Yet, countless savers keep building an emergency fund designed for a high-overhead lifestyle they left behind five years ago.

The Netflix Argument: Pure Survival vs. Family Stability

There is a fierce debate in the money management world about what a “bare-bones” budget should look like during a crisis. One school of thought says you should be utterly ruthless: if the hammer drops, you instantly cancel every streaming service, yank the kids out of gymnastics, stop eating out, and live strictly on beans and rice. It looks fantastic on paper.

But human beings do not live inside Excel files.

Consider the psychological impact on your kids. Children are hyper-aware of household tension. They might not understand macroeconomic downturns or corporate down-sizing, but they absolutely notice when their world suddenly shrinks and every familiar family routine disappears.

An emergency fund isn’t just about keeping the lights on; for parents, its truest value lies in purchasing a sense of normalcy when things go wrong. Keeping your kid in soccer or maintaining Friday pizza night during a rough patch isn’t a wasteful luxury. It is a direct investment in their emotional stability.

The Hidden Danger of Hoarding Too Much Cash

While the internet loves to worship aggressive savers, leaving mountains of cash sitting around comes with a brutal opportunity cost.

[Excess Cash in Bank] ➔ Short-Term Comfort but Long-Term Wealth Erosion (Inflation Drag)

[Cash Deployed in Markets] ➔ Short-Term Volatility but Long-Term Financial Freedom

Every single dollar over-allocated to a basic savings account is a dollar that isn’t compounding in a brokerage account, buying index funds, or acquiring real assets. Cash gives you short-term comfort, but long-term investing gives you actual freedom. Ironically, hoarding too much money out of an obsession with maximum security can end up tanking your financial security down the road.

So, when is an emergency fund “enough”?

A safety net is large enough when it successfully insulates you against realistic, real-world risks without completely freezing your progress toward your long-term wealth goals. For a dual-income couple renting an apartment, three months is plenty. For a self-employed dad with a mortgage and three kids, twelve months might be what it takes to sleep at night.

The perfect number depends entirely on your unique liabilities, not a generic rule from a textbook. If your bank account is stacked and you still feel terrified, stop checking your balance and look inward. Ask yourself: “What specific disaster am I trying to prevent?”

Because if you are trying to heal an emotional wound with a financial tool, another $15,000 isn’t going to fix it. True confidence doesn’t come from chasing an ever-moving target on a screen; it comes from knowing your risks, accepting that uncertainty is a part of life, and recognizing that one bad chapter does not mean the book is over.

External Regulatory Resources

For structural guidelines on banking safety thresholds and calculating accurate regional living costs, visit the Consumer Financial Protection Bureau Emergency Savings Resources and read the consumer protection materials provided by the FDIC Consumer Savings Guidance.

Disclaimer

The information provided in this article is for educational, informational, and entertainment purposes only. It does not constitute professional financial, investment, legal, or tax advice. Financial strategies, including emergency fund allocation, debt payoff methods, and investment strategies, vary greatly based on individual circumstances. Past performance of any strategy or investment vehicle is not indicative of future results. Content on this platform is not tailored to any specific individual’s financial situation. Before making any major financial decisions, consult with a certified financial planner (CFP), registered investment advisor (RIA), or qualified tax professional to evaluate your unique risk tolerance and financial goals.