A paid-off house feels like a finish line. No mortgage, no landlord, no monthly payment eating into your income. For a lot of retirees, it’s the single biggest financial win of their lives — and they’re right to feel good about it.

But a paid-off home is not a retirement plan. It’s an asset that doesn’t generate income, doesn’t cover groceries, and won’t write the check when the furnace dies in January. A surprising number of people arrive at retirement with exactly this setup: house paid off, Social Security coming in, maybe a modest 401(k), and not much else. And for a while, it looks fine on paper.

Then they run the actual numbers.

The $4,000 a Month Question

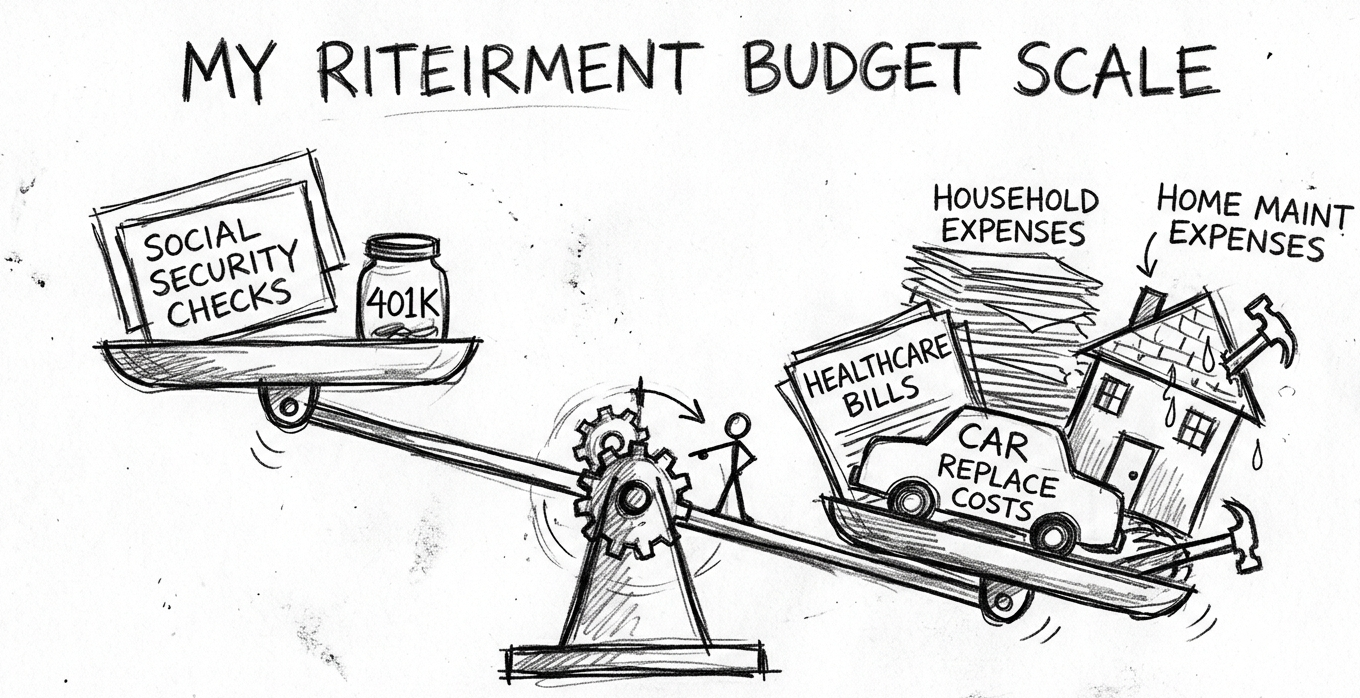

Social Security for a couple who both worked mid-wage jobs tends to land somewhere between $3,500 and $5,000 combined per month. That’s real income. And if there’s no mortgage, it goes further than people expect.

But “going further” is not the same as “going far enough.”

Take a couple bringing in $4,000 a month from Social Security, with $160,000 in a 401(k) and a paid-off home in a low-cost Midwestern city. No debt. No car payments. And somehow, they’re spending $4,500 a month. The $500 gap doesn’t sound catastrophic until you realize there’s no savings buffer, no investment growth covering that gap, and a list of future expenses — car replacement, roof repair, healthcare — that haven’t shown up yet.

This is the position a lot of retirees are actually in. Not broke. Not comfortable. Just thin.

What “Simple Lifestyle” Can Hide

When people describe their spending as simple, they usually mean it feels simple. No European vacations, no country club memberships, no boat payments. But feelings about spending and the actual numbers have a way of diverging.

$4,500 a month with no mortgage, in a low cost-of-living area, means roughly $54,000 a year in expenses. That’s not poverty — but it’s also not simple. For context, the Bureau of Labor Statistics’ Consumer Expenditure Survey puts average annual spending for adults 65 and older at around $52,000. So these aren’t extravagant numbers, but they’re average numbers for people who often do have mortgages and more demands on their income.

When spending is that high without those big fixed costs, it usually means smaller discretionary spending has filled the gap — dining out frequently, subscription services, gift-giving, convenience spending. None of it feels like luxury in the moment. All of it adds up.

The useful exercise is not to judge the spending but to categorize it: what’s fixed, what’s variable, and what could actually be cut without meaningfully changing how life feels day to day. Most households find they can trim 10–15% fairly quickly once they go line by line. That’s $450–$675 a month in this example — enough to tip the balance from breaking even to building a small buffer.

Social Security Is More Durable Than People Think — and Less Flexible

One thing that gets undersold: Social Security has a built-in inflation adjustment called the Cost-of-Living Adjustment (COLA), tied to the Consumer Price Index. In years with high inflation, it increases. That’s meaningfully different from a fixed pension or a savings account earning low interest.

For a retiree drawing most of their income from Social Security, inflation is less of a slow erosion than it is for someone pulling from a fixed account. The COLA won’t track medical inflation perfectly — healthcare costs tend to run hotter than general CPI — but it provides more protection than most people realize.

What Social Security doesn’t do is flex when you need more. If expenses spike — a car replacement, a medical procedure, a new HVAC system — you can’t call the SSA and ask for a bigger check that month. That’s where savings matter, even modest ones. The 401(k) isn’t just a retirement income source; it’s the emergency fund, the car fund, and the gap-filler for everything Social Security doesn’t cover.

At $160,000, a 4% annual withdrawal rate produces about $6,400 a year — roughly $533 a month. That’s not nothing, but it’s also not a lot of room when a decent used car costs $18,000 and assisted living averages over $4,500 a month nationally, according to the Genworth Cost of Care Survey.

The Cabin Problem (It’s Not Really About the Cabin)

A lot of families in this situation have some version of a cabin — a second property, a vacation home, something inherited that carries sentimental weight and real carrying costs. The family wants to keep it. The math is uncomfortable. And everyone is hoping Airbnb makes it work.

Short-term rental income is real, but it’s seasonal, inconsistent, and comes with costs that don’t show up in the optimistic version of the plan. Platform fees on Airbnb run 3–5%, plus cleaning between guests, maintenance, insurance riders for short-term rentals, and the occasional extended vacancy. A cabin in a northern lake region might see actual demand for four months out of twelve. If carrying costs are $1,200 a month, that’s $14,400 a year you need to net from rentals just to break even — before setting anything aside for repairs.

It can work. But the decision shouldn’t be “let’s try it and see.” It should start with a realistic income estimate from someone who knows that specific rental market, followed by an honest conversation about what happens if the numbers fall short.

If the property eventually needs to be sold to cover retirement expenses anyway, every year spent subsidizing it just reduces what’s left.

Inheritance Doesn’t Count Until It’s in the Bank

Planning retirement around an expected inheritance is common, and it introduces a specific kind of fragility. Life insurance policies lapse. Estate situations get complicated. Medical costs can consume assets faster than families expect, even with good coverage. Beneficiary designations change.

None of that means an inheritance won’t arrive. Sometimes it does, on schedule, in the expected amount. But a plan that only works if the inheritance comes through is really two plans — one that works and one that doesn’t. A fee-only financial planner will model both scenarios and show what the gap actually looks like over 20 years. That’s worth doing before committing to a cabin Airbnb strategy that’s funded, in part, by money that isn’t there yet.

Healthcare Is Where the Budget Gets Tested

Medicare Part B premiums in 2024 run $174.70 per person per month — that’s the floor. Add a Medigap supplemental policy and Part D drug coverage, and a couple can easily be spending $700–$900 a month on premiums alone, before any copays or out-of-pocket costs.

For a spouse who hasn’t reached 65 yet, marketplace coverage through the ACA is the option. Premium tax credits are income-based, and lower-income retirees often qualify for meaningful subsidies — but it requires actively shopping coverage on healthcare.gov each year and paying attention to how income changes (Roth conversions, part-time work, capital gains) can affect eligibility.

One thing worth knowing: traditional Medicare — Parts A and B — has no annual out-of-pocket maximum. That protection only comes with a Medicare Advantage plan or a Medigap supplemental policy. For retirees without substantial savings, that distinction is not minor.

What “Breaking Even” Costs You Over Time

Month-to-month balance is not security. A retiree couple spending exactly what they take in has no buffer for irregular expenses, no ability to absorb a down year in their investment account, and no margin for the increased healthcare and assistance costs that tend to show up in the mid-to-late 70s.

The goal isn’t unlimited savings. Most people don’t have that. The goal is enough margin that one bad thing — one car, one health event, one major repair — doesn’t force a larger decision about selling the house or moving in with the kids.

For a household in this position, that margin comes from three places: getting monthly expenses clearly below income, keeping the 401(k) intact as long as possible rather than treating it as a checking account, and making a clear decision about any secondary property before it becomes an obligation that’s hard to unwind.

A single session with a fee-only CFP will typically cost $200–$500 and produce an actual retirement projection — inflation included, healthcare modeled, withdrawal scenarios laid out. The NAPFA directory at napfa.org is the right place to find one. It won’t make the choices easier. But it will show exactly what each choice costs.

Owning your home outright is a genuinely strong position. It just isn’t the whole plan.

Financial Disclaimer

The information provided in this article is for informational, educational, and entertainment purposes only and should not be construed as professional financial, legal, or tax advice. We do not guarantee the accuracy or completeness of the information provided or the content of third-party external links. Always consult with a licensed, certified financial planner or fiduciary before making major investment or retirement decisions.