I walked out of my Fidelity retirement planning meeting feeling like I’d failed at adulting.

That’s not an exaggeration. I’m 43. I’ve got $350,000 sitting in a rollover Roth from an old job, another $10,000 in my current 401k, and I’m socking away 15% of my $140K salary every single paycheck. In my head, that’s “doing the responsible thing.” That’s “the boring middle-class dream, on track.” That’s what every personal finance podcast tells you to do.

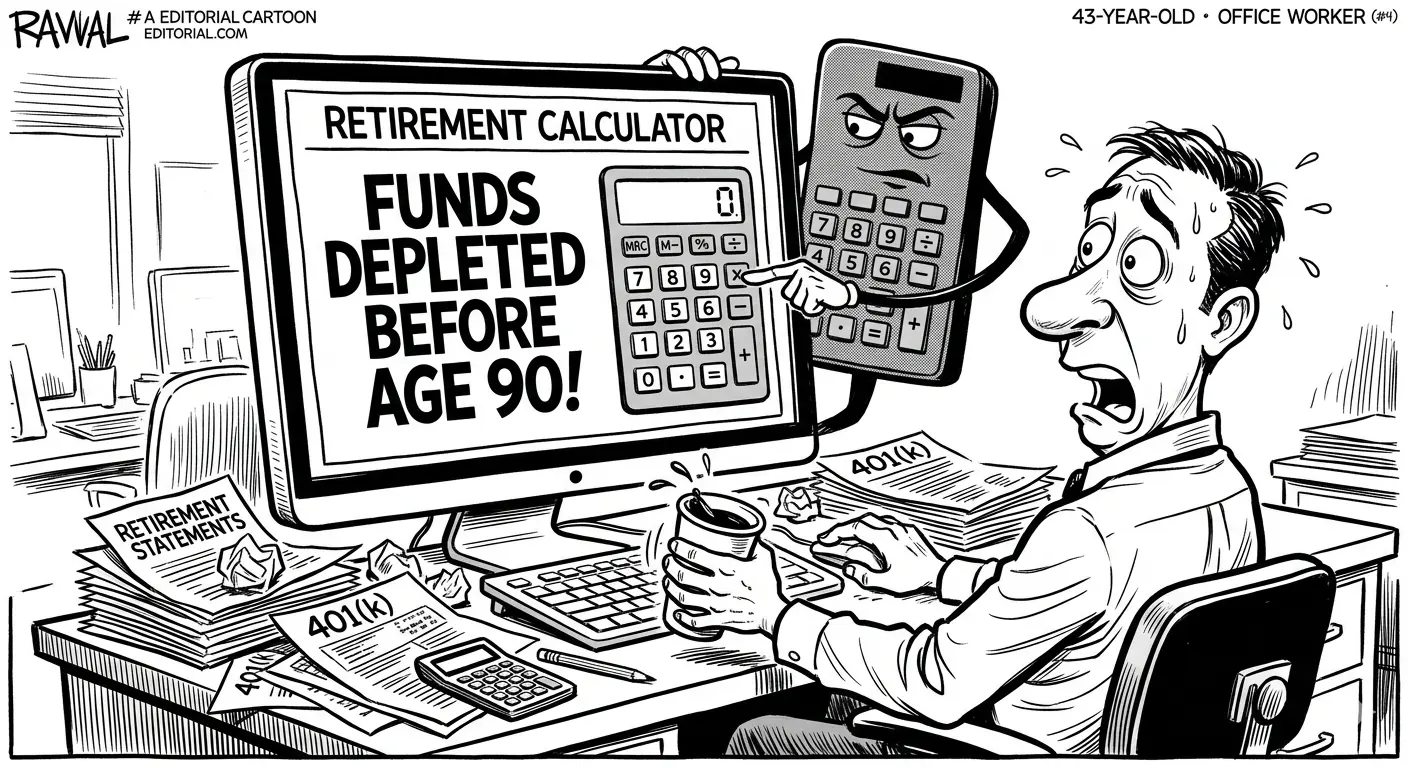

Then the Fidelity calculator looked me dead in the eye and said: cool story, but you’re going to run out of money before you turn 90.

I sat there blinking at the screen like it had just told me my dog wasn’t real.

If you’ve ever had a moment like this — where a number on a screen made your stomach drop and made you question every financial decision you’ve made since college — keep reading. Because what I found out afterward changed how I think about these calculators completely, and it might do the same for you.

Wait, Am I Actually Behind on Retirement Savings?

Here’s the thing nobody tells you walking into one of these meetings: that scary number isn’t really a prediction. It’s closer to a fire drill.

I went down a rabbit hole after my appointment (anxiety will do that to you), and it turns out the Fidelity retirement calculator doesn’t show you what’s likely to happen. By default, it shows you something closer to a worst-case scenario. According to Fidelity’s own methodology, when you run the planner, it executes 250 simulations based on historical returns and displays three scenarios: Significantly Below Average Market, Below Average Market, and Average Market. The “Significantly Below Average” option — the one that probably made your eye twitch — means that 90% of historical return scenarios actually end up doing better than what you’re looking at, and Fidelity specifically recommends using that conservative scenario for planning purposes.

Translation: the calculator basically asked, “what if the market tanks for the rest of your life and you have the worst possible luck,” and then showed you that result like it was the forecast. No wonder I left feeling like I needed to go lie down in a dark room.

I wasn’t the only one who didn’t know this. I posted about my experience on r/personalfinance, half expecting people to tell me I was cooked. Instead, I got an avalanche of “hey, same thing happened to me” and “here’s what you’re missing.”

The Comments Section Saved My Sanity (And Maybe My Retirement)

One commenter did the math out loud and it stopped me cold: “Something isn’t adding up in your calculations — 350k should go to roughly 1.5 million in that time period with zero additional contributions, with normal investing strategy.” In other words, my existing balance alone — without adding one more dollar — was already projected to grow into the exact number that scared me. The “you’ll run out of money” part wasn’t about me not having enough. It was about the calculator assuming a brutal, below-average 22 years in the market on top of conservative withdrawal assumptions.

Another person broke down the actual mechanics of how Fidelity scores you. Your “Retirement Preparedness Measure” gets calculated under those same gloomy market assumptions, and it represents the percentage of your average estimated retirement expenses your plan could potentially cover, assuming a significantly below average market. So even people who are objectively crushing it can get a less-than-stellar score, simply because the tool is built to stress-test you against bad luck, not show you the most probable outcome.

That’s when the lightbulb went off for me. This wasn’t a verdict. It was a stress test. And I’d been treating a stress test like a prophecy.

So Why Does the Calculator Make Everyone Panic?

Honestly? I think it’s by design — and not in a sinister way. A calculator that only ever shows you sunshine and double-digit returns isn’t doing you any favors. If the market crashes the year before you retire (ask anyone who was 64 in 2008), you want to have already planned for that. Conservative-by-default is a feature, not a bug.

But — and this is the part that nobody explains in the meeting — there’s a real cost to that design choice: it scares the daylights out of regular people who are actually doing fine. One Redditor put it bluntly: “Fidelity is great as a discount brokerage but their advisor services and retirement calculator are not very good. Stop using these.” Strong opinion, but I get the frustration behind it.

Another commenter who works with Fidelity advisors regularly (helping manage a parent’s accounts) explained it this way: the projections shown in these meetings are typically “what happens if the markets perform significantly below average” — and that selection is adjustable, sitting right there on the website under your account, but most people never realize they can toggle it to see the “Average Market” scenario instead.

I went back and checked. They were right. There’s a dropdown. A literal dropdown that I didn’t touch during my entire appointment.

What I Actually Did Next (And What You Should Check Too)

I’m not a financial advisor, and neither is your cousin who “made a killing in crypto,” so take this as one regular person sharing what worked, not gospel. But here’s my post-panic action list:

1. I checked which market scenario I was looking at. Like I mentioned — there’s a toggle. Comparing “Significantly Below Average” against “Average Market” completely changed the picture for me.

2. I double-checked my inputs. Did I actually enter my current contribution rate? My real salary? Did I forget to add future Social Security income? One small missing input can throw the whole projection sideways. Several Redditors pointed out that people often forget to layer in things like Social Security start dates, mortgage payoff dates, or Medicare transitions — all of which the tool lets you customize but defaults to ignoring.

3. I ran my numbers through a second, independent calculator. Multiple commenters recommended cross-checking with other tools instead of relying on one company’s projection. This is honestly just good practice — would you trust one doctor’s opinion for a major diagnosis without a second opinion? Same energy here.

4. I looked at the math in plain English. Twenty-two more years of consistent 15% contributions, plus compound growth on $360K, plus whatever Social Security I’m eventually owed? That’s a very different story than “you’ll be broke at 90.”

5. I stopped treating one tool as gospel. This was the big mental shift. The calculator is a flashlight, not a fortune teller. It shows you one possible path in the dark, not the only path.

The Real Lesson Here (It’s Not About the Money)

If there’s one thing this whole experience taught me, it’s that financial anxiety doesn’t always come from actually being behind. Sometimes it comes from misreading a tool that was never designed to comfort you in the first place.

I’m not saying “ignore the warning and YOLO it.” If a calculator flags a real gap, that’s useful information and worth taking seriously. But before you spiral, it’s worth asking: what assumptions is this tool making, and have I actually checked them?

Because here’s the kicker — I’m still going to bump my contributions up. Not because I’m drowning, but because now I actually understand the lever I’m pulling, instead of blindly reacting to a scary screen. That’s the difference between fear-driven decisions and informed ones.

If you’ve had a similar gut-punch moment with a retirement calculator, you’re in very good company. A whole comment section of strangers on the internet had my back — turns out the internet is occasionally good for something other than doom-scrolling.

A Couple of Resources Worth Bookmarking

- Social Security Administration — create your account to see your actual projected benefit in today’s dollars. This single number changes a lot of these calculations.

- Fidelity’s own published methodology on how the retirement planner’s market scenarios work is worth a skim if you want the nerdy details straight from the source.

Disclaimer: I’m not a licensed financial advisor, and nothing in this article is personalized financial, investment, tax, or legal advice. It’s one person’s experience and general information for educational purposes only. Retirement calculators rely on assumptions that may not reflect your actual situation, and past market performance doesn’t guarantee future results. Before making major financial decisions, please consult a qualified, licensed financial advisor who can look at your full picture.