Here is something that will absolutely blindside most people who are planning to retire early: a man who stopped working at 40 years old — not 65, not 62, forty — is sitting on a projected $45,000 per year in Social Security benefits the moment he turns 70. His wife, with a nearly identical earnings history, stacks on another $45,000. Combined, that is $90,000 a year in guaranteed, inflation-adjusted income landing in their bank account every single year for the rest of their lives — covering nearly every non-discretionary expense they have. And neither of them has paid a dime into Social Security since the day they walked out of their offices.

If you just blinked and reread that sentence, you are not alone.

Most people planning an early retirement mentally file Social Security under “things that probably won’t apply to me.” A ghost payment from a government program for people who worked until they were 65. Something your grandparents collected. Not something relevant to someone retiring in their 40s with an investment portfolio doing the heavy lifting.

And that belief — right there — might be the single most expensive miscalculation in the society.

Here is what nobody tells you upfront: the Social Security formula is not designed the way most people think. It is not a piggy bank. It is not proportional. And the dirty little secret hiding inside the math is that high earners who retire early are accidentally one of the biggest beneficiaries of how the formula actually works.

Why the “Just Ignore It” Strategy Is Quietly Costing People Years of Their Lives

Walk into any financial independence forum and you will find two camps when it comes to Social Security. Camp One ignores it entirely, treating it as a mythological benefit that will almost certainly be gutted, privatized, or means-tested into oblivion before they ever collect a check. Camp Two factors it in at full value without ever questioning whether the system will look the same in 30 years.

Both camps are making a mistake.

The people ignoring it are leaving a massive, legally entitled income source completely off their retirement balance sheet — and as a result, they are working longer than they have to. One person ran their FIRE numbers for years without factoring in Social Security and found they would have to work until their mid-60s. When they plugged in a conservative 60% of their projected benefit, their retirement date moved forward by nearly a decade.

That is not a rounding error. That is close to ten years of their life.

The people counting on it at full value are carrying real risk, especially younger earners who are 30 to 40 years away from eligibility. A lot can change in four decades. Assuming the full projected benefit shows up exactly as calculated is optimistic in a way that could genuinely hurt you if the math shifts.

The answer, as with most things in personal finance, is somewhere in the middle — and it requires actually understanding how Social Security early retirement benefits are calculated, not just guessing.

The Formula That Almost Nobody Understands

Here is the assumption that quietly destroys people’s Social Security math: they think the system works like a bank account. Work 35 years, collect proportionally. Work 18 years, collect about half. Stop early, get crushed.

Wrong.

The Social Security benefit formula is deliberately, aggressively weighted toward your first dollars of lifetime earnings. The government built it this way on purpose to protect lower-income workers who spent decades earning modest wages. But here is the beautiful and largely unannounced irony: that same progressive design structure also massively benefits high earners who stop working early.

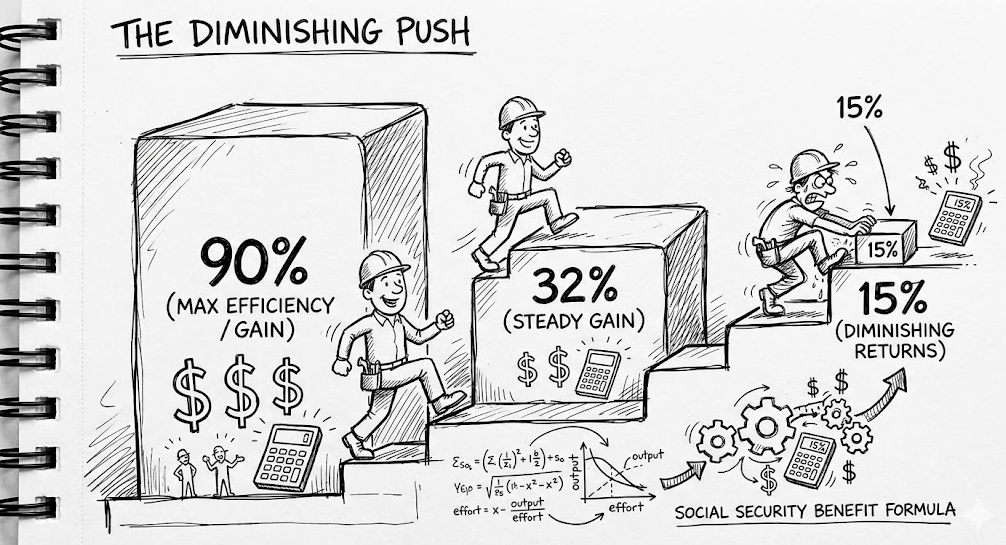

The formula works like this. Social Security takes your top 35 years of earnings, adjusts each year for wage inflation, averages them together to produce what’s called your AIME (Average Indexed Monthly Earnings), and then applies a tiered formula with two key thresholds called bend points.

In 2026, those bend points work roughly like this:

- The first $1,226 of your monthly AIME gets credited back to you at 90 cents on the dollar

- Everything between $1,226 and $7,391 per month gets credited at 32 cents on the dollar

- Everything above $7,391 per month gets credited at just 15 cents on the dollar

What does that mean in human terms? If you spent your 20s and 30s maxing out your Social Security contributions — the wage cap in 2026 is $184,500 — you already burned through that 90% zone early in your career. You are deep into the 32% zone. Adding more years of maximum contributions barely changes your eventual benefit because those additional dollars are being credited at the lowest possible rate.

The math rewards your first years of high earnings far more than it rewards year 20, year 25, or year 30.

This is why one person who retired at 37 — with 17 or 18 years of zero contributions stretching out ahead of them — calculated that stopping work that early only reduced their eventual Social Security benefit by roughly 23% compared to if they had kept working at the same salary for another two full decades.

Seventeen years of zeroes. Twenty-three percent reduction.

That is the number that changes how you think about this.

The Second Bend Point: The Invisible Finish Line

There is a specific milestone hiding inside the Social Security formula that almost nobody knows about until they stumble across it.

It takes roughly 17 to 18 years of maxing out Social Security contributions to hit what is called the second bend point — the threshold where your additional earnings start returning only 15 cents on every dollar. Once you cross that line, the marginal value of every additional year you work, from a pure Social Security perspective, is minimal.

So if you graduated college at 22, worked aggressively, hit the wage cap in your late 20s or early 30s, and kept maxing it out — you may have crossed the second bend point somewhere around age 40 to 45. At that moment, every additional year of work you do for Social Security purposes is returning a fraction of a cent in future benefits per dollar contributed.

That is not a reason to stop working if you love what you do or if your portfolio needs the runway. But it is a reason to stop letting the Social Security calculation be the thing that keeps you tethered to a job you are ready to leave.

The best free tool for visualizing exactly where you stand on the bend point curve is ssa.tools — a third-party calculator that lets you input your actual earnings history, model zero-income years, and see your projected benefit at 62, 67, and 70 side by side. It is genuinely one of the most useful and underrated retirement planning tools on the internet.

The Real Scenario That Started This Conversation

Let me walk you through the actual earnings history that produced that $45,000 projection, because the details matter.

- Graduated college in 2008

- First real income: roughly $60,000 that year

- Income climbed steadily each year as the career progressed

- Hit the Social Security wage maximum of $117,000 in 2014

- Maxed the wage cap every single year through 2026 — 12 consecutive years at the ceiling

- Plans to stop working entirely at age 40

- Plans to start collecting Social Security at age 70

That is not 35 years of maximum contributions. That is 18 years of actual earnings — 6 at or near the cap and 12 at the full maximum — followed by 17 zeroes averaged into the 35-year calculation.

And the result is still projected to be $45,000 per year in today’s dollars at age 70.

Some people in the financial independence community pushed back hard on this number and said the math did not work. What they missed is that the formula does not just care about the 12 years at the maximum. It also counts those 6 earlier years of solid and climbing income. That combination — 18 years of real, substantial earnings, 6 of which approached or hit the cap — pushes the AIME number high enough to land just at or near the second bend point.

The result? A Social Security benefit that, when combined with a spouse in a similar position, covers nearly all of their household fixed expenses at 70. Meanwhile, the investment portfolio they built in their 20s and 30s has been compounding quietly for three decades, completely untouched.

“But Will Social Security Even Exist When I Get There?”

This is the question every person under 45 is screaming at the screen right now. Fair.

Here is the honest, non-hysterical answer.

The Social Security trust fund is currently projected to face a funding shortfall in the early 2030s. If Congress does absolutely nothing between now and then — which, to be clear, would be politically extraordinary — benefits would need to be reduced across the board by roughly 20 to 25% to match incoming payroll tax revenue. That is the actual doomsday number from the nonpartisan Social Security actuaries. Not zero. Not 50%. About one-fifth.

But Congress doing absolutely nothing on Social Security is about as likely as Americans voluntarily giving up their tax refunds. Social Security has roughly 70 million current beneficiaries and hundreds of millions more who are counting on it. It is the third rail of American politics for a reason. Every senator and representative in Washington either is currently collecting Social Security, will be soon, or has parents and constituents who depend on it for survival.

The proposed fixes that show up most consistently in nonpartisan policy discussions include: raising or eliminating the wage cap on contributions, adjusting the formula for very high earners, modestly raising the full retirement age, and making a slightly higher portion of benefits taxable for upper-income recipients. None of those scenarios results in Social Security disappearing for early retirees. Several of them actually improve the system’s long-term solvency significantly.

There is also the means-testing question — the one that genuinely worries people who have saved aggressively. Could Congress decide that high-net-worth retirees do not need their Social Security benefit and reduce it for them? It is possible. Politically, it is a complicated move because it effectively penalizes people for having saved responsibly. But it cannot be completely ruled out over a 30-year time horizon.

Here is what multiple savvy FIRE-minded people have noted about means-testing, though: if your investment portfolio is doing its job over 30 years, you probably will not need the Social Security check to survive anyway. And if your portfolio fails catastrophically — extended bear market, sequence-of-returns disaster, unexpected expenses — you probably will not have the assets that trigger a means test. It is somewhat self-correcting for the people who plan carefully.

The practical planning approach most financially independent people land on: model your Social Security at 70 to 75% of your projected benefit. That is conservative enough to account for likely adjustments without being so pessimistic that it forces you to work an extra decade for an income source you are legally entitled to. If the full benefit shows up, you get a bonus. If adjustments happen, you already planned for it.

Some people go more conservative — 50 to 60% — if they are very young (early 30s or younger) and have a 35-plus year horizon before eligibility. That is also reasonable. The further out you are, the more uncertainty you are carrying.

What is not reasonable, statistically or mathematically, is planning around zero.

The Age 70 Decision: Why Patience Is Worth 24% More Money

Here is a number that deserves its own paragraph.

Every year you delay claiming Social Security past your full retirement age (currently 67 for anyone born in 1960 or later), your eventual monthly benefit grows by approximately 8%. Wait from 67 to 70, and you have locked in a 24% permanent increase in your monthly payment. For the rest of your life. Inflation-adjusted annually.

There is no low-risk financial product in America that pays 8% annually with zero downside.

For someone retiring in their 40s, this is almost a non-decision. You are not touching Social Security for 20-plus years anyway. Your investment portfolio has decades of growth ahead of it. The only question is whether you claim at 62 (the earliest possible age, with a permanent reduction), at 67 (your full retirement age, no reduction), or at 70 (maximum benefit, 24% above full retirement age).

For early retirees, the case for waiting until 70 is strong. The payment that starts at 70 is not just larger — it functions as longevity insurance. If you live to 85, 90, or beyond, that inflation-adjusted monthly check becomes increasingly critical as the real purchasing power of everything else fluctuates. The breakeven analysis on waiting past 62 typically hits around the mid-to-late 70s. The average 62-year-old today can expect to live well into their 80s.

The goal of Social Security, as one thoughtful person framed it, is not to maximize total lifetime payout. It is to eliminate the risk of running out of money if you live a very long time. That is the insurance function. You are not trying to win a game. You are trying to make sure that if you are 91 years old and the market has had three bad years in a row, you still have a guaranteed income floor that covers your basics.

That framing changes the whole claiming strategy conversation.

The Married Couple Playbook: One Early, One Late

For married couples, the Social Security claiming strategy gets more nuanced — and more powerful.

The general approach that financial planners and retirement researchers most commonly recommend: the lower earner files early (around age 62) while the higher earner waits until 70.

Here is why the math supports this.

The lower earner’s Social Security benefit is essentially an annuity that pays from the day they claim until whichever spouse dies first. The higher earner’s benefit, on the other hand, is a payment that continues until the last surviving spouse dies — because when the higher earner passes away, the surviving spouse can switch to the higher earner’s benefit amount as a survivor benefit.

That survivor benefit can be up to 100% of the deceased spouse’s payment. Which means the higher earner’s delayed, 24%-larger benefit does not just protect them personally. It becomes the financial floor for whoever is left behind.

If you are the higher earner in your household, delaying to 70 is not just about your retirement. It is about making sure your spouse has a substantial guaranteed income if they outlive you by 10 or 20 years — which statistically, there is a real chance they will.

There is a meaningful exception to this framework. If both spouses have very similar earnings histories — close to the same income for most of their careers — the picture shifts. In that case, many retirement planners recommend that both spouses wait as long as possible, since neither has a dramatically higher benefit to protect the other.

If this all feels like a lot of variables, the free tool OpenSocialSecurity.com runs the joint optimization calculation for couples. You input both partners’ earnings histories and ages, and it spits out the claiming ages that maximize your combined lifetime expected benefit. It accounts for survivor benefits, the age gap between spouses, and life expectancy. It is worth 20 minutes of your time.

The Hidden Tax Goldmine Between Ages 65 and 70

Here is one of the most underappreciated retirement planning insights available to early retirees — and it lives in a five-year window most people never think about.

If you retire early and delay Social Security until 70, you have a roughly five-year span — from age 65 (when Medicare eligibility begins) to age 70 (when Social Security starts) — where your taxable income is almost entirely in your hands. No required distributions yet. No Social Security income pushing your bracket higher. Just you and your portfolio.

That window is the sweet spot for Roth conversions.

You can take money from your traditional IRA or 401(k) — where it grows tax-deferred but will eventually be taxed on withdrawal — and convert chunks of it to a Roth IRA, where it will grow completely tax-free forever. During those five years, you can stay within the 12% or 22% federal tax bracket, pay a modest tax bill today, and eliminate future tax liability on that money permanently.

Why does Social Security timing matter here? Because once your Social Security check starts arriving, up to 85% of your benefit becomes taxable income. That additional income pushes your converted Roth amounts into higher brackets. The move that cost you 22 cents on the dollar at age 67 might cost you 32 cents on the dollar at age 72. The five-year window before Social Security starts is when the conversion math is most favorable.

Retirement researchers and financial planners who work with early retirees call this the “Social Security tax torpedo” — the sharp spike in effective tax rate that hits when Social Security income collides with IRA withdrawals and required minimum distributions. Planning your Social Security claim date with this window in mind can save meaningful money over a 20 to 30 year retirement.

This is also why some financially independent people with large traditional retirement accounts actually prefer to delay Social Security as long as possible — not because they need the income, but because the delay funds a bigger Roth conversion runway.

The One Rule That Trips Up Fast-Track Earners

Here is a detail that genuinely trips up the small percentage of people who hit very high incomes quickly and plan to retire before their early 40s.

To qualify for any Social Security retirement benefit, you need 40 work credits. In 2026, you earn one credit for approximately $1,890 of income, with a maximum of four credits per year. Simple math: you need income in at least 10 separate years to qualify.

For most people reading this, that is already checked off. Summer jobs in high school, work-study in college, a few years of adulting before the real career started — most people have 20 to 30 credits before they even land their first real job.

But for the rare person who hit an extremely high income very quickly out of school — a startup equity event, a few years in finance or medicine, an early exit — it is worth logging into ssa.gov and confirming your credit count is at least 40.

If you are a few credits short, the fix is genuinely inexpensive. A small amount of self-employment income, properly reported and taxed, earns you four credits in a year. The self-employment tax rate is 15.3%, so earning around $8,000 in a year covers your four annual credits and costs you roughly $1,200 in taxes. That is a very cheap insurance premium when you consider what it unlocks — both the eventual Social Security retirement benefit and, critically, free Medicare Part A coverage for life. Hospital coverage that would otherwise cost over $500 per month during the years you are not yet eligible for Medicare at 65.

For people who plan to access healthcare through the Affordable Care Act marketplace during early retirement, qualifying for Medicare Part A eventually matters a lot. Confirm your credits. It takes five minutes.

How Ignoring Social Security Distorts Your Number

There is a specific and understandable reason why the FIRE community developed a culture of ignoring Social Security in retirement projections. When you are trying to retire at 35 or 40, Social Security is 22 to 30 years away. It feels irrelevant to the immediate planning problem, which is: do I have enough invested right now to cover my expenses for the next three decades?

That math has to work without Social Security, because Social Security cannot save you in year 5 of retirement if your portfolio falls apart.

But here is what gets missed: ignoring Social Security does not just make your plan more conservative. It often makes your plan wrong in a way that costs you years of unnecessary work.

Consider a high-earning couple, both planning to retire in their mid-40s, projecting combined retirement expenses of $10,000 per month. Their FIRE number — using the standard 4% withdrawal rate — would be roughly $3 million. That is what they build toward.

Now factor in that at 70, conservatively, this couple might project $5,000 to $6,000 per month in combined Social Security income in today’s dollars. That income, arriving guaranteed for the rest of their lives, effectively reduces the portfolio withdrawal needed to cover their expenses by 50 to 60%.

Their actual FIRE number, accounting for Social Security as a future income floor, is not $3 million. It might be $2 million or less — depending on how aggressively they want to model the Social Security income and what withdrawal rate they apply to the years before it starts.

That gap represents years of a person’s working life. Years that could have been spent doing something else.

The way most careful FIRE planners handle this is to run two parallel calculations: a base plan that works without any Social Security at all, and a secondary projection that shows what the numbers look like with a conservative Social Security estimate factored in. The base plan tells you the worst case. The secondary plan tells you how much cushion you are actually building.

Both numbers are useful. Only looking at one of them is not.

What to Actually Do This Week

Here is the specific action list, in priority order:

Step 1: Create your mySocialSecurity account. Go to ssa.gov and set up a free account. Pull your full earnings history. Every year you worked should be there, with the actual dollar amount reported. Verify it is accurate. Errors are more common than people think, and old records from early jobs are the most likely to be missing or wrong. Disputing an error gets harder the older it is.

Step 2: Change your future income assumption to zero. Inside your mySocialSecurity account, look for the Annual Income section. You can change the default assumption — which is “you’ll keep earning what you earned last year until you retire” — to $0. That gives you the honest early retirement projection. See what your estimated benefit looks like at 62, 67, and 70 under that assumption.

Step 3: Run your numbers at ssa.tools. The official ssa.gov calculator is useful but limited. ssa.tools allows you to input your actual historical earnings year by year, model future zero-income years, and see a visual chart of your projected benefit across multiple claiming ages. It shows you exactly where you land relative to the bend points. Spend 20 minutes here and you will understand your Social Security picture better than most financial advisors’ clients do.

Step 4: For couples, run the joint optimization. Go to opensocialsecurity.com and run the calculation for both partners. It accounts for survivor benefits, spousal benefits, your age gap, and life expectancy tables. It typically takes about 10 minutes and usually confirms the lower earner claims early / higher earner waits to 70 strategy — but your specific numbers may produce a different result.

Step 5: Build Social Security into your FIRE number — conservatively. Take your projected benefit at 70 from ssa.tools with future income set to zero. Multiply that number by 0.75 (your conservative adjustment for potential future changes). That is your Social Security planning number. Build a secondary retirement projection that shows how your required portfolio withdrawal changes once that income floor arrives at 70. The gap between your base plan and this adjusted plan is the true picture of your retirement cushion.

The Bottom Line

Social Security early retirement benefits are not a footnote for people who plan to leave the workforce in their 40s. They are not a wishful-thinking bonus that probably won’t exist. And they are definitely not something you should write off because you stopped contributing years before traditional retirement age.

For high earners who built a serious income during their 20s and 30s, the Social Security benefit formula’s progressive structure already captured the majority of your eventual payment during those first 15 to 18 years of work. The additional years you might grind through simply to “maximize” Social Security are largely returning 15 cents on the dollar anyway.

Meanwhile, that $45,000-per-year projection — or whatever your equivalent number is — represents a guaranteed, inflation-adjusted income floor that no market crash can touch, no sequence-of-returns disaster can erode, and no longevity risk can outlast.

The couple sitting on $90,000 in combined projected Social Security income at 70 did not find a loophole. They did not get lucky. They just understood how the math actually works — and they stopped letting a myth about early retirees and Social Security add unnecessary years to their working lives.

Go log into ssa.gov this week. Run your actual numbers. You probably get more than you think.

And if that number — even at 75% — materially changes your FIRE timeline, you owe it to yourself to know that before you spend another year at a desk.

This article is intended for general educational and informational purposes only. It does not constitute financial, tax, or legal advice. Social Security rules, benefit formulas, and eligibility requirements are established by federal law and may be changed by Congress at any time. Benefit projections discussed here are illustrative and based on publicly available information from the Social Security Administration. Your actual benefit will depend on your individual earnings history, claiming age, marital status, and applicable law at the time you claim. Before making any decisions about Social Security claiming strategy, retirement income planning, or investment allocation, consult with a certified financial planner (CFP), registered investment advisor (RIA), or qualified tax professional who can evaluate your specific situation.